10-K: Annual report [Section 13 and 15(d), not S-K Item 405]

Published on March 19, 2026

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM 10-K

_________________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2025

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ___________ to ___________

Commission file number 001-42813

_________________________

(Exact name of registrant as specified in its charter)

_________________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of Principal Executive Offices) | (Zip Code) | |||||||

(212 ) 891-2880

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

☐ | Smaller reporting company | |||||||||||||

Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

The registrant was not a public company as of June 30, 2025, the last business day of the registrant’s most recently completed second fiscal quarter. Therefore, the registrant cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such date. The registrant’s Common Stock began trading on the Nasdaq on September 15, 2025.

As of March 18, 2026, the registrant had 11,196,169 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement for the registrant’s 2026 Annual Meeting of Stockholders, expected to be filed pursuant to Regulation 14A within 120 days from December 31, 2025, are incorporated by reference into Part III of this Annual Report on Form 10-K to the extent stated herein.

Table of Contents

3

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. Forward-looking statements reflect the Company’s current views with respect to, among other things, capital resources, portfolio performance and results of operations. Likewise, the Company’s consolidated financial statements and statements regarding anticipated growth in its operations, anticipated market conditions, demographics and results of operations are forward-looking statements. In some cases, you can identify these forward-looking statements by the use of terminology such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words or phrases.

The forward-looking statements contained in this Annual Report on Form 10-K are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that it has anticipated. Actual results may differ materially from those in the forward-looking statements. Some factors that could cause the Company’s actual results to differ include:

•the risk that any synergies from the Business Combination (as defined herein) may not be fully realized or may take longer to realize than expected;

•the risk of litigation related to the Business Combination;

•variability in revenues, earnings, and cash flows and the resulting impact on quarterly earnings trends and stock price volatility;

•the intensity of competition in asset management and insurance markets and constraints on the ability to execute growth strategies and maintain or increase market share or margins;

•reliance on technology and information systems, including third party and systems provided by BC Partners Advisors L.P. (“BCPA”), and risks related to cybersecurity, data integrity, and operational resilience;

•dependence on management’s assumptions, estimates, models, and judgment, and the risk that actual outcomes diverge materially from those assumptions;

•illiquidity of certain assets under management and insurance investments, and the impact of limited liquidity on valuation, portfolio management, and capital allocation;

•dependence on access to financing markets and the availability, cost, and terms of capital and liquidity;

•risks associated with the use of hedging and other risk management instruments, including costs, basis risk, counterparty exposure, and potential ineffectiveness;

•adverse political, market, and economic conditions and their effects on investment performance, funding costs, client activity, and policyholder behavior;

•dependence on BCPA and key BCPA personnel;

•actual and potential conflicts of interest arising from the relationship with BCPA;

•concentration risk associated with managing a limited number of funds and investments;

•complexities and subjectivity in valuing illiquid assets, including model risk and sensitivity to assumptions;

•the heavily regulated nature of the insurance business; and

•the increased expenses and compliance requirements associated with being a U.S. public company.

These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Company’s control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the section entitled “Item 1A. Risk Factors” of this Annual Report on Form 10-K. Should one or more of these risks or uncertainties materialize, or should any of the assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Unless the context otherwise requires, (i) all references in this Annual Report on Form 10-K following the closing of the Business Combination on September 12, 2025 to “we,” “us,” “our,” the “Company,” and “Mount Logan” refer to Mount Logan Capital Inc. (formerly, Yukon New Parent, Inc.), as the registrant, and its consolidated subsidiaries and (ii)

4

all references prior to the closing refer to Legacy Mount Logan (as defined herein). The Mount Logan logo and our other registered or common law trademarks, service marks, or trade names appearing in this Annual Report on Form 10-K are the property of Mount Logan Capital Inc. Other trade names, trademarks, and service marks used in this Annual Report on Form 10-K are the property of their respective owners.

5

PART I

Item 1. Business

Formed in 2018, we are a publicly traded, alternative asset management and insurance solutions company that is focused on public and private debt securities in the North American market and the reinsurance of annuity products, primarily through our wholly-owned subsidiaries Mount Logan Management LLC (“ML Management”) and Ability Insurance Company, a Nebraska domiciled insurer (“Ability”), respectively. We also actively source, evaluate, underwrite, manage, monitor and primarily invest in loans, debt securities, and other credit-oriented instruments that present attractive risk-adjusted returns and present low risk of principal impairment through the credit cycle. We conduct our business primarily in the United States through our two business segments: Asset Management and Insurance Solutions.

On September 12, 2025 (the “Closing Date”), the Company completed a business combination pursuant to an Agreement and Plan of Merger, dated as of January 16, 2025 and amended as of July 6, 2025 and August 17, 2025 (the “Merger Agreement”) among the Company (formerly, Yukon New Parent, Inc.), Mount Logan Capital Inc., a corporation organized under the laws of the Province of Ontario (“Legacy Mount Logan”), and 180 Degree Capital Corp. (“TURN”), a New York corporation that was registered as a closed-end investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”), Polar Merger Sub, Inc., a corporation organized under the laws of the State of New York and wholly owned subsidiary of the Company (“TURN Merger Sub”), and Moose Merger Sub, LLC, a limited liability company formed under the laws of the State of Delaware and a wholly owned subsidiary of the Company (“MLC Merger Sub”) wherein (i) TURN Merger Sub. merged with and into TURN, with TURN surviving as a wholly owned subsidiary of the Company, and (ii) MLC Merger Sub merged with and into Legacy Mount Logan, with Legacy Mount Logan surviving as a wholly owned subsidiary of the Company (collectively, the “Business Combination”). Following the completion of the Business Combination, the Company changed its name from “Yukon New Parent, Inc.” to “Mount Logan Capital Inc.” and became a Nasdaq-traded public company. The Business Combination was accounted for as a reverse acquisition, with Legacy Mount Logan identified as the accounting acquiror and the legal acquiree.

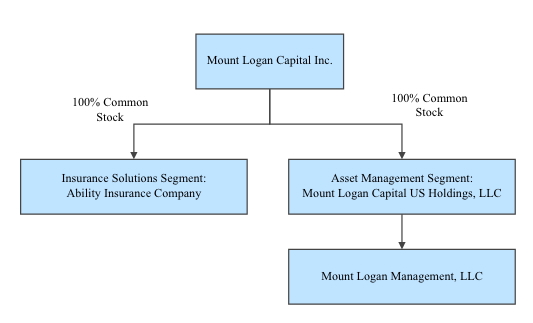

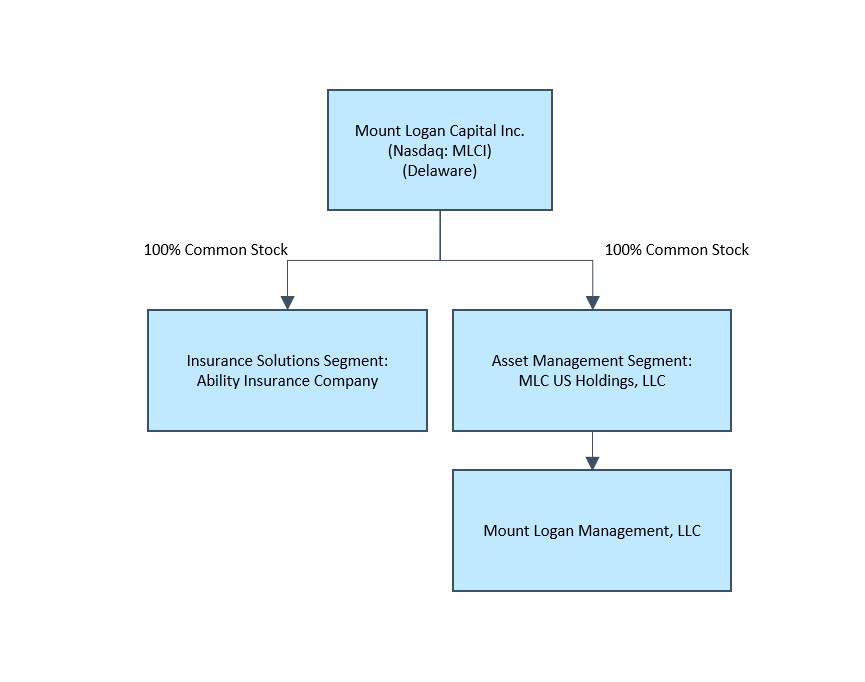

The diagram below depicts Mount Logan’s current organizational structure:

Our Businesses

Asset Management

Our Asset Management segment focuses on private credit across senior secured lending, asset-based and specialty finance, structured and opportunistic credit, venture and growth lending, and select equity-linked solutions. We provide origination, underwriting, portfolio construction and risk management to a diversified client base, including insurance accounts, a BDC platform, our interval funds (SOFIX, ACIF), Separately Managed Accounts (“SMAs”) and other vehicles. We manage substantially all of the assets of Ability, our primary Insurance Solutions business, and maintain an active dialogue with the insurance solutions team.

For these services, we generate recurring fee streams across a diversified set of credit investing strategies. After expenses required to generate our fee revenues, the remaining profit stream constitutes Fee Related Earnings (“FRE”), our primary performance measure for this segment. We operate the platform integrated with our insurance solutions business, enabling collaboration on sourcing and asset allocation aligned to similarly-dated liabilities.

6

Our investment philosophy is centered around deploying capital into well-established middle-market businesses that operate across a wide range of industries, while limiting concentration in any one industry. We employ fundamental credit analysis, targeting investments in businesses with relatively low levels of cyclicality and operating risk. We seek to provide a full credit cycle investment offering, with the ability to opportunistically allocate capital to fill the white space created as other capital sources retrench. As part of our opportunistic allocation of capital, we are able to underwrite complex, less competitive niches, and deploy capital during periods of uncertainty with a consistent emphasis on downside protection and preservation of capital. Many of our mandates utilize multi-year, permanent or semi-permanent capital, allowing us to invest patiently across the capital structure, scale AUM, and compound recurring FRE through cycles. As of December 31, 2025, we had total AUM in excess of $2.1 billion.

We have experience managing levered vehicles, both public and private, and seek to enhance returns through the prudent use of leverage with a conservative approach that prioritizes downside protection and capital preservation. We believe this strategy and approach offers attractive risk-adjusted returns with lower volatility given the potential for fewer defaults and greater resilience through market cycles.

Permanent or Semi-Permanent Capital

Included within our investing strategies above is $1.5 billion of permanent or semi-permanent capital, out of the over $2.1 billion of total AUM, as of December 31, 2025. As of December 31, 2025, permanent capital includes, without limitation, certain assets in our credit strategy, including assets relating to publicly traded and non-traded vehicles, and assets managed for certain of our Insurance Solutions clients, which have indefinite or long-term investment horizons, and in specific cases provide stable sources of funding while allowing for liquidity access for investors through redemption mechanisms. We do not include vehicles with definite term, finite investment periods, or funds that are in wind-down in our definition and aggregation of permanent or semi-permanent capital.

The amount of fees charged for managing these assets depends on the underlying investment strategy, vehicle being managed, liquidity profile, and, ultimately, our ability to generate returns for our clients. After expenses associated with generating fee-related revenues, we measure the resulting earnings stream’s “Fee Related Earnings” or “FRE”, which represents the primary performance measure for the Asset Management segment. FRE is the sum of all recurring fees underpinned by asset management activities including but not limited to: (i) management and servicing fees, (ii) interest income attributable to investment management activity, (iii) equity investment earnings related to fee generating vehicles, and (iv) fee-related performance fees from certain managed funds with indefinite terms, measured and received on a recurring basis and not dependent on realization events of the underlying investments, less (x) fee related compensation expense, excluding equity-based compensation, and (y) other associated operating expenses, which excludes growth investments into the retail distribution platform, amortization of acquisition-related intangible assets, interest and other credit facility expenses, foreign exchange-related gains and losses, and other non-recurring, nonmaterial items that are not required for the management of the underlying assets and investments.

Historically, we focused on strategic acquisitions and partnerships to expand our asset management capabilities, including but not limited to (i) the 2020 transaction alongside SCIM, whereby SCIM became the investment advisor to the Alternative Credit Income Fund (“ACIF”), (ii) the purchase of, and subsequent increase in, a minority stake in SCIM, which manages Portman Ridge Finance Corp. (“PTMN”), a closed-end, externally managed, non-diversified investment company that has elected to be treated as a Business Development Company (“BDC”) under the Investment Company Act of 1940, (iii) the 2021 acquisition of certain assets from Capitala Investment Advisors, LLC, whereby ML Management became the manager of Logan Ridge Finance Corp. (formerly Capitala Finance Corp.) (“Logan Ridge”), also a BDC, and (iv) the transaction with Ovation Partners, LP (“Ovation”), for the management of its alternative income platform, which included the transfer of employees to ML Management to support its specialty finance and asset-backed finance efforts across commercial lending, real estate lending, consumer finance, and litigation finance.

The Asset Management segment also holds minority equity interests in (i) Runway Growth Capital, LLC (“Runway”), which is a private credit, SEC-registered investment adviser managing $1.2 billion AUM with a specific orientation on providing growth capital to sponsored (i.e., venture-backed) and non-sponsored companies, and (ii) two Canadian alternative asset managers focused on investment grade, high yield, private credit, and asset-backed investment strategies. The minority investment in Runway Growth Capital was acquired during the first quarter of 2025 by Legacy Mount Logan, but for purposes of this filing is not considered a significant investment in accordance with Rule 3-09 of Regulation S-X.

We are differentiated by the scale, depth, diversity, and investment performance of our funds and investment solutions. The diversity of our credit products and private market solutions demonstrates our focus on expanding and enhancing our capabilities, in support of investment performance on behalf of our investment clients. We believe the

7

achievement of attractive risk-adjusted returns will continue to support growth in AUM and the recurring fee streams it earns across the vehicles it manages.

Insurance Solutions

We acquired Ability in the fourth quarter of 2021. Today, Ability is a Nebraska domiciled reinsurer of annuity products that specializes in reinsuring annuity products for the increasing number of individuals seeking to fund retirement needs. Upon closing of the acquisition of Ability, ML Management entered into an investment management agreement with Ability (the “Ability IMA”) to manage certain of Ability’s assets that are within the scope of ML Management’s expertise in providing investment management advisory services (the assets of Ability managed by ML Management are referred to herein as the “Managed Ability Portfolio”). Ability then shifted the focus of our insurance business away from legacy insurance products, and reoriented around retirement solutions products, including multi-year guaranteed annuities (“MYGA”). Ability’s long-term goal is to build a platform that can both insure and reinsure a diverse set of competitive annuity and life insurance products.

Our acquisition of Ability combined two products that we believe are, and will continue to be, in high demand – insurance solutions and alternative asset management. We, through our acquisition of Ability, brought the insurance business additional capital to support growth, a stronger investment portfolio through ML Management’s repositioning of the portfolio, stability and continuity of liability management, and new growth opportunities that we believe will provide increased security to policyholders. The acquisition positioned us for a new stage of growth, as the stronger capital base and alignment allows us to scale asset and liability origination for the benefit of Ability’s policyholders as well as us and our shareholders.

We are focused on generating spread income, or Spread Related Earnings (“SRE”), within our Insurance Solutions segment for the benefit of policyholders, through (i) sourcing long-term liabilities and (ii) using the origination and investment capabilities of our Asset Management segment to source or originate assets that fit Ability’s targeted risk and return characteristics. SRE represents the difference between actual earnings generated on the assets and investments made and the interest or crediting rate guaranteed to policyholders or participants. We view SRE as a critical measurement for assessing the profitability of the Insurance Solutions segment, as it excludes the impact of certain market volatility and other one-time, non-core components of income or loss. Rather than increasing allocations to higher risk securities to increase yields, or returns, on the assets invested, Ability and ML Management focus on proprietary origination of high-quality, predominantly senior secured loans and assets, which we believe reduces downside risk. SRE is a key financial metric that we defined and report as a non-GAAP financial measure. See “—Segment Analysis—Insurance Solutions” for a reconciliation of SRE to the most directly comparable U.S. GAAP measure.

Our asset management expertise supports the sourcing and underwriting of assets for Ability’s portfolio. Ability is invested in a diverse array of high-grade fixed income assets including corporate bonds, structured securities and commercial real estate loans, as well as senior secured loans. Ability manages its interest rate risk through hedging activity to lower its overall net floating rate position. Ability also maintains holdings in less interest rate-sensitive investments, including CLOs, non-agency residential mortgage-backed securities (“RMBS”), and various types of structured products, consistent with its strategy of pursuing incremental yield by assuming liquidity and complexity risk, rather than assuming incremental credit risk.

Ability’s Products

Ability currently reinsures annuity products, consisting of MYGA, and is licensed in 42 states and the District of Columbia. We acquired Ability in the fourth quarter of 2021. As part of the transaction, we invested $10 million of capital into Ability to strengthen its balance sheet and launch a platform for the reinsurance of annuities. The reinsurance of annuity products commenced in the second quarter of 2022. As of December 31, 2025 we have contributed an incremental $37.2 million of capital and investments into Ability.

Annuities are a contract with an insurer where individuals agree to pay a certain amount of money, either in a lump sum or through installments, which entitles them to receive a series of payments at a future date. MYGA products are single premium deferred individual annuity contracts, providing consumers with an attractive, low-risk, predictable, and tax deferred investment option.

Effective April 1, 2022, we, through Ability, closed a reinsurance agreement with Atlantic Coast Life Insurance Company (“ACL”) pursuant to which Ability assumed a 20% quota share coinsurance of up to $150.0 million of premium of MYGA policies beginning January 1, 2021. Effective July 1, 2022, Ability closed on an additional reinsurance agreement with Sentinel Security Life Insurance Company (“SSL”) to assume a 20% quota share coinsurance of up to $100.0 million of premium of MYGA policies. These quota share coinsurance agreements were met as of July 10, 2023. On January 10, 2024, we, through Ability, amended the reinsurance agreements with ACL and with SSL, pursuant to

8

which Ability would assume a 20% quota share coinsurance of premium of MYGA policies issued and approved on or after October 1, 2023. Ability elected to terminate the amended reinsurance agreements, effective June 30, 2024, to diversify and grow liability origination away from the initial counterparties, ACL and SSL. On March 31, 2025, Ability entered a new reinsurance treaty for additional MYGA with National Security Group (“NSG”), further diversifying its reinsurance partners.

Ability has a runoff book of long-term care (“LTC”) business, which we classify as Ability’s legacy business. Ability has several reinsurance agreements to reinsure the long-term care portfolio's morbidity risk. Ability is no longer insuring new long-term care risk. The last LTC policy Ability wrote was in the early 2000’s, and thus, LTC has not been a core focus of the insurance business for multiple decades.

Reinsurance Channels

Ability is focused on reinsurance through quota-share agreements in the form or flow or block trades, as well as acquisitions, which supports Ability’s liability origination efforts across market environments. As Ability continues to grow, it remains disciplined in its evaluation of liabilities that are core to its strategy.

Capital

Ability believes it has a strong capital position and is well positioned to meet policyholder and other obligations, which it determines through various internal capital metrics tracked by management. The amount of capital required to support Ability’s core operating strategies is determined based on internal modeling and analysis of economic risk, as well as inputs from rating agency capital models and consideration of National Association of Insurance Commissioners (“NAIC”) risk-based capital (“RBC”) requirements. Capital in excess of this required amount is considered excess equity capital, which is available to deploy.

Ability’s Market Opportunity

Ability participates in a large U.S. market that it expects to grow in part due to several demographic trends. As measured by annual premiums written, annuities are the largest product line in the life and annuity sector. Annuities play an important role in retirement planning by providing individuals with stable, tax-efficient sources of income. In 2025, annuity premiums totaled $461.3 billion, up 6% year over year, accordingly to preliminary results from LIMRA’s U.S. Individual Annuity Sales survey, which represents 92% of the U.S. annuity market. The most common annuities are fixed and variable and may be written on an individual or group basis. The current products Ability reinsures are fixed annuities written on an individual basis.

There is an increasing demand for retirement solutions as a growing portion of the U.S. population is of retirement age and the retirement income needs of retirees are expected to increase. The number of people of retirement age has increased significantly since 2010, driven by the aging of the “Baby Boomer” generation. The U.S. population over 65 years old is forecast to grow from 57.8 million in 2022 to an estimated 78.3 million in the next 20 years, according to the U.S. Census Bureau, Population Estimates and Projections. This study also forecasted that the U.S. population aged over 65 years old is expected to grow by 44% from 2020 to 2040, while the total U.S. population is expected to grow by only 12%. Currently, 17.3% of the U.S. population is 65 or older, which is projected to rise to 22% by 2040, according to the ACL. The UN’s Population Statistics group has also forecasted that the global population aged 65 and over is expected to double from 0.8 billion to 1.6 billion, increasing from 10% to 17% of the total population, by mid-century. This demographics-driven demand has been further supported by a higher interest rate environment, which has enabled annuity providers to enhance their product offerings with more attractive crediting rates, strengthening the overall value proposition for consumers.

Annuities play an increasingly vital role in retirement planning, offering retirees stable, tax-efficient, and guaranteed income streams. In 2025, total fixed-rate deferred annuity sales reached $160.6 billion, improving by 5% since 2024. The consistent growth in MYGA demand has been a key driver of the overall expansion in the fixed annuity market. Ability’s current product focus is centered on individual MYGA offerings, where Ability sees continued opportunity for growth.

Growth Strategy

We are building a diversified alternative asset management and insurance solutions platform. With the completion of the Business Combination and our Nasdaq listing, we believe we have improved access to the capital markets, improved financing flexibility and a stronger balance sheet to accelerate organic and inorganic growth initiatives. Our team’s priorities include (i) investing into Ability to support increased reinsurance flows to expand Ability’s liabilities and investment portfolio to generate positive SRE, primarily managed by our registered advisor, ML Management; (ii) scaling

9

our private credit AUM across existing and future vehicles to increase FRE; and (iii) selective acquisitions and partnerships that broaden origination, diversify products, and enhance operating leverage. These initiatives are intended to reinforce shareholder value by compounding FRE and SRE via a capital flywheel. As assets under management increase, FRE rises, generating additional cash flow at the parent company. We can reinvest this cash into Ability to support new reinsurance treaties, which expand liabilities and invested assets. These assets generate SRE while also increasing AUM managed by Mount Logan, which in turn produces more FRE and cash flow to be re-deployed. We pursue this growth within a framework of disciplined underwriting, regulatory compliance, and capital management.

Asset Management

Our objective is to become a fully diversified private credit manager for institutional, retail and insurance clients. We are growing AUM in existing vehicles, new strategies, and through accretive acquisitions and partnerships that add capital and incremental origination channels. We intend to: (i) expand AUM in our existing vehicles; (ii) launch adjacent strategies that can scale through our distribution network; and (iii) pursue acquisitions or partnerships that add origination and recurring fees. These initiatives are supported by our permanent and semi-permanent capital base and our track record managing diverse investment vehicles. We are capitalizing on secular tailwinds as banks continue to re-trench and private credit fills the gap. We evaluate new vehicle launches, acquisitions and partnerships based on a number of factors including: (i) strategic fit (e.g. credit capability expansion, distribution); (ii) durability of capital (i.e. permanent or semi-permanent capital, what we refer to as “sticky AUM”); (iii) underwriting culture, risk controls, and unit economics (e.g., FRE uplift and margin accretion); and (iv) ease of integration into our operating model, as supported by our Staffing and Resource Agreement and Servicing Agreement (each as defined below) with BCPA.

Insurance Solutions

We are scaling a capital-efficient insurance platform pairing long-dated, predictable liabilities with our private credit origination and underwriting capabilities. A strengthened balance sheet following our combination with 180 Degree Capital positions us to grow our insurance capabilities. Our objectives include:

Expand MYGA Reinsurance Through Diversified Channels: Our Insurance Solutions segment, through Ability, is initially focused on MYGA reinsurance, a product with fixed tenors, high predictability, and strong growth in the fixed annuity market. We intend to increase our cadence of quota-share flow treaties and opportunistic blocks with a broader set of counterparties, building on previously executed agreements. Any new reinsurance treaties we enter into will be filed with and approved by appropriate state insurance regulatory authorities before being executed.

Increase our RBC Ratios via Direct Investments from Mount Logan, compounding SRE and Reinforcing the Asset Management “Flywheel”: Mount Logan as Parent can invest capital directly into Ability to support MYGA reinsurance and other insurance activities that we may pursue in the future. Through our asset management segment, we target attractive spread economics and active portfolio management to optimize Ability’s assets, while earning a management fee for performing these activities. The flywheel between asset management and insurance solutions is a key driver of the compounding growth of our business.

Broaden Product Set and Strengthen Distribution: Over time we plan to expand beyond MYGA into complementary retirement and life protection solutions, including fixed indexed annuities and pre-need products, subject to market conditions and regulatory approvals. We also plan to diversify and expand its liability based through flow and block transactions where attractive opportunities arise, complementing its direct writing capabilities. As scale increases across products and distribution channels, we expect to drive improved operating leverage, enhance the durability of SRE, and maintain disciplined management of asset-liability matching, RBC ratios, and regulatory capital.

Competition

Asset Management

Competition is high in the asset management industry, and more specifically the alternative asset management space in which we primarily operates. We face competition from a large number of asset managers that focus on the management of public and private funds, as well as commercial and investment banks, merchant banks, commercial financing companies, institutional investors, insurance companies and, to the extent they provide an alternative form of financing, private equity funds.

With respect to our investment strategies and the deployment of capital, we primarily compete with other private markets solutions providers within North America and Europe that specialize in private credit. We endeavor to maintain strong relationships with general partners and other alternative asset managers who manage investment funds, as well as the general investment community that can include investment banks, commercial banks, advisors, brokers, legal firms, and

10

accountants. Our non-sponsored, or non-private equity-backed, deals are sourced through a proprietary and robust network of industry contacts and other channels including existing relationships with owners or management teams of middle market companies, family-owned businesses, and niche industry players. We view the non-sponsored channel as less competitive given the wide dispersion of opportunities across North America and Europe, which are harder to source, evaluate, and underwrite. However, because of the increasing demand for private credit investments and growth across the industry, there can be no assurance that we will be able to invest all of the capital it raises in investments that meet our risk-adjusted return thresholds, or that the size of investment opportunities available to us will meet our investment sizing targets.

To grow our business, we must compete for investor capital, both within our existing investor base and the broader investor universe that is actively seeking to deploy capital into the private markets, and specifically funds managed by alternative asset managers like ML Management. Historically, our ability to raise additional capital, and thus grow AUM, is based on a variety of factors, including but not limited to:

•Investment performance across our managed and sub-advised investment strategies;

•Ability to originate and execute private credit investment opportunities;

•Nature and duration of investor relationships;

•Quality of service;

•Fund terms, including fees;

•Brand recognition of the platforms through which we operate as well as the brand recognition of the firms which we partner with, including BCPA and Runway;

•Ability to customize product offerings to fit our institutional, retail, and insurance client specifications; and

•Ability to provide cost effective and comprehensive range of services and products.

Competition is also high to attract and retain highly qualified investment professionals and support functions personnel. Our ability to continue to compete effectively within our industry will depend upon our ability to attract new employees and to motivate and retain our existing employees.

Insurance Solutions

We operate in a highly competitive industry through our Insurance Solutions operating subsidiary, Ability. Ability reinsures annuity products, which compete with fixed rate, fixed index, and variable annuities sold by other insurance companies and also with mutual fund products, traditional bank products, and other investment and retirement funding alternatives offered by other asset managers, banks, and broker/dealers.

The products Ability reinsures may compete with products of other insurance companies, financial intermediaries and other institutions based on several features, including crediting rates, index options, policy terms and conditions, ratings, reputation, and distributor compensation.

Many of Ability’s competitors are well-established, and have greater market share, broader networks, and maintain financial strength ratings from A.M. Best, which Ability does not have today. Larger competitors can have lower operating costs, enabling them to participate in transactions at more competitive pricing levels for insurance products, reinsurance solutions, and acquisitions. This pricing pressure could affect our Insurance Solutions segment’s ability to maintain or increase profitable growth. Ability has primarily grown through MYGA block reinsurance transactions and flow reinsurance, and increased competition within these insurance products could impact transaction pricing, potentially challenging future growth.

Regulatory and Compliance Matters

Our businesses, as well as the financial services and insurance industries generally, are subject to extensive regulation in the United States and around the world. Virtually all aspects of our business are subject to various laws and regulations, some of which are summarized below. Under these laws and regulations, agencies that regulate investment advisers, investment funds, insurance businesses, and other individuals and entities have broad administrative powers, including the power to limit, restrict, or prohibit the regulated entity or person from carrying on business if it fails to

11

comply with such laws and regulations. Failure to comply with applicable regulatory and compliance requirements may result in a variety of consequences, including fines; administrative measures; suspension of voting rights; suspension of individual employees; limitations on engaging in certain lines of business for specified periods of time or mandatory disposal of interests in any affected regulated entity; revocation of investment adviser, insurance, and other registrations; licenses, or charters; censures; and other regulatory sanctions. The legal and regulatory requirements applicable to our business are ever evolving and may become more restrictive, which may make compliance with applicable requirements more difficult or expensive, or otherwise restrict our ability to conduct our business activities in the manner in which they are now conducted. our businesses have operated for many years within a legal framework that requires being able to monitor and comply with a broad range of legal and regulatory developments that affect our activities. However, additional legislation, changes in rules promulgated by self-regulatory organizations, or changes in the interpretation or enforcement of existing laws and rules, either in the United States or elsewhere, may directly affect our mode of operation and profitability. The complex regulatory frameworks governing financial institutions, insurance companies, and insurance distributors and their respective holding companies and subsidiaries, as well as those with investments in them, are very detailed and technical. Accordingly, the discussion below is general in nature, does not purport to be complete and is current only as of the date of this Annual Report on Form 10-K.

Regulation under the Advisers Act

We conduct our advisory business primarily through ML Management and SCIM, each of which is registered as an investment adviser with the SEC under the Advisers Act. ML Management and SCIM are subject to, among other Advisers Act provisions, the anti-fraud provisions of the Advisers Act and to fiduciary duties derived from these provisions, which apply to the RIA’s relationships with their advisory clients globally, including funds that the RIAs manage. These provisions and duties impose restrictions and obligations on the RIA with respect to their dealings with their fund investors and their investments, including for example restrictions on agency cross and principal transactions. ML Management and SCIM are subject to periodic SEC examinations and other requirements under the Advisers Act and related regulations primarily intended to benefit advisory clients. These additional requirements relate, among other things, to maintaining an effective and comprehensive compliance program, record-keeping and reporting requirements and disclosure requirements. The Advisers Act generally grants the SEC broad administrative powers, including the power to limit or restrict an investment adviser from conducting advisory activities in the event it fails to comply with federal securities laws. Additional sanctions that may be imposed for failure to comply with applicable requirements include the prohibition of individuals from associating with an investment adviser, the revocation of registrations, and other censures and fines.

Insurance Regulation

Ability is subject to extensive regulation and supervision by the states in which it is domiciled, particularly with respect to their financial condition. Ability is domiciled in Nebraska, where it is regulated and supervised by the Nebraska Department of Insurance (“NEDOI”). Ability is also subject to regulation by all states in which the company transacts business; oversight that, in practice, often focuses on review of Ability’s market conduct. Ability is licensed to conduct insurance business, and is therefore subject to regulation and supervision by insurance regulators, in 42 states and the District of Columbia.

The extent and scope of insurance regulation varies between jurisdictions, but most jurisdictions have laws and regulations governing the financial security of insurers, including admittance of assets for purposes of calculating statutory surplus, standards of solvency, reserves, reinsurance, capital adequacy, and the business conduct of insurers.

In addition, statutes and regulations require the licensing of insurers and their agents, the approval of policy forms and related materials, and the approval of rates. State statutes and regulations also prescribe the permitted types and concentrations of investments by insurers. The primary purpose of this insurance industry regulation is to protect policyholders. Life insurance companies are required to file detailed quarterly and annual financial statements with insurance regulatory authorities in each of the jurisdictions in which they are licensed to do business, and their operations are subject to periodic examination by such authorities. Regulators have discretionary authority, in connection with the continued licensing of insurance companies, to limit or prohibit the insurance company’s ability to continue to do business if, in their judgment, the regulators determine that an insurer is not maintaining necessary statutory surplus or capital or if the further transaction of business will be detrimental to its policyholders.

The amount of dividends that Ability may pay in any twelve-month period, without prior approval by its domestic insurance regulator, is restricted under the laws of Nebraska.

We, an insurance holding company, together with our insurance subsidiary, Ability, are subject to the insurance holding company system laws of Nebraska. These laws generally require insurers that are members of such insurance holding company’s system to register with the jurisdiction’s insurance regulatory authorities, to file reports disclosing

12

certain information, including the insurance holding company’s capital structure, ownership, management, financial condition, enterprise risk, and own risk and solvency assessment.

These laws also require disclosure of certain qualifying transactions between Ability and any of our other subsidiaries or affiliates. Such transactions could include loans, investments, sales, service agreements, and reinsurance agreements among other similar inter-affiliate transactions. These laws also require that intercompany transactions be fair and reasonable and not adversely affect the interests of policyholders. In certain circumstances, the insurance company must give prior notice of the transaction to the insurance department in its state of domicile, and the insurance department must either approve or disapprove the subject intercompany transaction within defined periods. Further, these laws require that an insurer’s surplus following any dividends or distributions to shareholder affiliates is reasonable in relation to the insurer’s outstanding liabilities and its financial needs.

The insurance holding company laws in some states, including Nebraska, require regulatory approval of a direct or indirect change of control of an insurer or an insurer’s parent company. Generally, to obtain approval from the insurance commissioner for any acquisition of control of an insurance company or its parent company, the proposed acquirer must file with the applicable commissioner an application containing information regarding:

(i)the identity and background of the acquirer and its affiliates;

(ii)the nature, source and amount of funds to be used to carry out the acquisition;

(iii)the financial statements of the acquirer and its affiliates;

(iv)any potential plans for disposition of the securities or business of the insurer;

(v)the number and type of securities to be acquired;

(vi)any contracts with respect to the securities to be acquired;

(vii)any agreements with broker-dealers; and

(viii)other relevant matters.

Different jurisdictions may have similar or additional requirements for prior approval of any acquisition of control of an insurance or reinsurance company licensed or authorized to transact business in those jurisdictions. Additional requirements may include re-licensing or subsequent approval for renewal of existing licenses upon an acquisition of control.

Statutory Examinations

Ability is required to file detailed quarterly and annual financial statements, prepared in accordance with statutory accounting practices (“SAP”), with regulatory officials in each of the jurisdictions in which they conduct business. As part of their routine regulatory oversight process, the NEDOI conducts periodic detailed examinations, generally once every three to five years, of the books, records, accounts and operations of Ability. The NEDOI began its regularly-scheduled examination of Ability for the period of 2020-2022 in August 2023, completing its examination and issuing its final report on October 25, 2024.

Financial Tests

The NAIC has developed a set of financial relationships or “tests,” known as the Insurance Regulatory Information System, or IRIS, which is designed for early identification of companies that may require special attention or action by insurance regulatory authorities. Insurance companies submit data annually to the NAIC, which in turn analyzes the data by utilizing ratios. State insurance regulators review this statistical report, which is available to the public, together with an analytical report, prepared by and available only to state insurance regulators, to identify insurance companies that appear to require immediate regulatory attention. A “usual range” of results for each ratio is used as a benchmark.

Risk-Based Capital Requirements

In order to enhance the regulation of insurers’ solvency, the NAIC has adopted a model law to implement RBC requirements for life insurers. All states have adopted the NAIC’s model law or a substantively similar law. The NAIC Risk-Based Capital Model Act requires insurance companies to submit an annual RBC Report, which compares an insurer’s total adjusted capital with its authorized control level RBC. A company’s RBC is calculated by using a specified

13

formula that applies factors to various specified assets, premium, claim, expense, and reserve items. The factors are higher for those items with greater underlying risk and lower for items with less underlying risk.

The RBC Report is used by insurance regulators to set in motion appropriate regulatory actions relating to insurers that show indications of weak or deteriorating conditions. RBC is an additional standard for minimum capital requirements that insurers must meet to avoid being placed in receivership by regulators. The annual RBC Report, and the information contained therein, is not intended by the NAIC as a means to rank insurers.

RBC is a method of measuring the minimum amount of capital appropriate for an insurance company to support its overall business operations in light of its size and risk profile. It provides a means of setting the capital requirement in which the degree of risk taken by the insurer is the primary determinant. The value of an insurer’s Total Adjusted Capital, which is the sum of its year-end statutory capital and surplus, in relation to its RBC, together with its trend in its Total Adjusted Capital, is used as a basis for determining regulatory action that a state insurance regulator may be authorized or required to take with respect to an insurer.

Ability is subject to RBC standards and other minimum capital and surplus requirements imposed by state laws. Regulatory capital requirements for Ability are determined in accordance with statutory requirements of the Nebraska Department of Insurance. The minimum RBC ratio for Ability is 200% and Ability must have a ratio in excess of 300% to be able to reinsure new business. Regulatory action is triggered beginning at 200% RBC and below. The regulatory action varies with risk based capital level as follows: (i) if a company’s total adjusted capital is less than 200% but greater than or equal to 150% of its authorized control level RBC, the company shall submit a risk-based capital plan to the regulatory authority highlighting conditions which contributed to lower adjusted capital and proposing corrective actions aimed at improving its capital position; (ii) if a company’s total adjusted capital is less than 150% but greater than or equal to 70% of its authorized control level RBC, the regulatory authority will perform such examination and analysis of the assets, liabilities, and operations including a review of its risk-based capital plan of the company as deemed necessary and issue an order specifying the corrective actions that must be taken; (iii) if a company’s total adjusted capital is less than 70%, the regulatory authority may take any action it deems necessary, including placing the company under regulatory control. Ability’s RBC ratio is tested annually at the end of Ability’s financial year and estimated on a quarterly basis.

Market Conduct Exams

Ability is subject to periodic market conduct exams (“MCE”) in any jurisdiction where it does business. An MCE typically entails review of business activities, such as operations and management, complaint handling, marketing and sales, producer licensing, policyholder service, underwriting, and claims handling. Regulators may impose fines and penalties upon finding violations of regulations governing such business activities.

Form Approvals

Ability is subject to state laws and regulations regarding form approvals. In most states, insurance policies are subject to prior regulatory approval in the state in which the policy is sold.

Unfair Claims Practices

Insurance companies are prohibited by state statutes from engaging in unfair claims practice. Unfair claims practices include, but are not limited to, misrepresenting pertinent facts or insurance policy provisions; failing to acknowledge and act reasonably promptly upon communications with respect to claims arising under insurance policies; and attempting to settle a claim for less than the amount to which a reasonable person would have believed such person was entitled.

Regulation of Investments

Ability is subject to state laws that restrict the kinds of investments it may make. These laws require diversification of investment portfolios and limit the amounts of investments in certain asset categories, such as below-investment grade fixed income securities, equity real estate, other equity investments, and derivatives. Failure to comply with these requirements and limitations could cause affected investments to be treated as non-admitted assets for purposes of measuring statutory surplus and, in some instances, could require the divestiture of such non-qualifying investments. Ability’s investment guidelines, including its Derivative Use Plan, have been filed with the NEDOI.

Statutory Accounting Practices

SAP are a basis of accounting developed to assist insurance regulators in monitoring and regulating the solvency of insurance companies. SAP is primarily concerned with measuring an insurer’s solvency. Statutory accounting focuses on

14

valuing assets and liabilities of insurers at financial reporting dates in accordance with appropriate insurance law and regulatory provisions applicable in each insurer’s domiciliary state.

U.S. GAAP is concerned with a company’s solvency, but is also concerned with other financial measurements, principally income and cash flows. Accordingly, U.S. GAAP gives more consideration to appropriately matching revenue and expenses and accounting for management’s stewardship of assets than does SAP. As a result, different assets and liabilities and different amounts of assets and liabilities will be reflected in financial statements prepared in accordance with U.S. GAAP as compared to SAP.

Enterprise Risk and other Developments

The NAIC, as part of its solvency modernization initiative, has engaged in a concerted effort to strengthen the ability of U.S. state insurance regulators to monitor U.S. insurance holding company groups. The holding company reform efforts at the NAIC culminated in December 2010 in the adoption of significant amendments to the NAIC’s Insurance Holding Company System Regulatory Act (the “Model Holding Company Act”) and its Insurance Holding Company System Model Regulation (the “Model Holding Company Regulation”). Among other things, the revised Model Holding Company Act and Model Holding Company Regulation explicitly address “enterprise” risk — the risk that an activity, circumstance, event, or series of events involving one or more affiliates of an insurer will, if not remedied promptly, be likely to have a material adverse effect upon the financial condition or liquidity of the insurer or its insurance holding company system as a whole — and require annual reporting of potential enterprise risk as well as access to information to allow the state insurance regulator to assess such risk. In addition, the Model Holding Company Act amendments include a requirement to the effect that any person divesting control over an insurer must provide 30 days’ notice to the regulator and the insurer (with an exception for cases where a Form A is being filed). The amendments direct the domestic state insurance regulator to determine those instances in which a divesting person will be required to file for and obtain approval of the transaction. Some form of the 2010 amendments to the Model Holding Company Act and the Model Holding Company Act Regulation has been adopted in all states.

Consumer Protection Laws and Privacy and Data Security Regulation

Federal and state consumer protection laws affect our operations. As part of the Dodd-Frank Act, Congress established the Consumer Financial Protection Bureau to supervise and regulate institutions that provide certain financial products and services to consumers. In addition, the Gramm-Leach-Bliley Act of 1999 implemented fundamental changes in the regulation of the financial services industry in the United States and includes privacy and security requirements for financial institutions, including obligations to protect and safeguard consumers’ nonpublic personal information and records, limitations on the re-disclosure and re-use of such information, and requirements to notify customers and other individuals about their policies and practices relating to their collection and disclosure of such information and their practices relating to protecting the security and confidentiality of that information.

In addition to federal and other financial institution-specific privacy laws and regulations, an increasing number of states are considering and passing comprehensive privacy legislation. The issues surrounding data security and the safeguarding of consumers’ protected information are under increasing regulatory scrutiny by state and federal regulators.

Employees

As of December 31, 2025, we had no employees. We rely on BCPA to provide us with certain management and administrative services. In addition, our senior management team is comprised of substantially the same personnel as the senior management of BCPA. BCPA, together with its affiliates, is a global alternative asset manager focused on private credit, private equity and real estate.

Since November 20, 2018, BCPA, as servicing agent (the “Servicing Agent”), performs (or oversees, or arranges for the performance of) the administrative services necessary for the operation of Mount Logan, including, without limitation, office facilities, equipment, bookkeeping and recordkeeping services and such other services as the Servicing Agent, subject to review by our Board, shall from time to time deem necessary or useful to perform its obligations under the servicing agreement (as amended from time to time, the “Servicing Agreement”). The Servicing Agreement, by its terms, is subject to annual approval by our board of directors. We pay the Servicing Agent an amount equal to our allocable portion of the Servicing Agent’s overhead resulting from its obligations under the Servicing Agreement, including rent and the allocable portion of the cost of our Chief Financial Officer and associated personnel. The Servicing Agent, from time to time, pays amounts owed by us to third-party providers of goods or services, and subsequently reimburse the Servicing Agent for such amounts paid on our behalf at cost.

On November 18, 2025, we and BCPA entered into a Staffing and Resource Agreement (the “Staffing and Resource Agreement” and together with the Servicing Agreement, the “BCPA Arrangements”), pursuant to which certain

15

designated BCPA employees provide services to us. The Staffing and Resource Agreement allows us and BCPA to share personnel for a variety of investment advisory activities. Pursuant to the Staffing and Resource Agreement, BCPA may allocate costs and expenses relating to the Staffing and Resource Agreement as agreed to between us and BCPA. The Staffing and Resource Agreement, by its terms, can be terminated upon sixty (60) days’ prior written notice to the non-terminating party or as otherwise mutually agreed between us and BCPA.

The BCPA Arrangements allow us to leverage BCPA’s infrastructure and scale, including the resources of BCPA’s credit team.

Available Information

Our website is located at www.mountlogancap.com and our investor relations website is ir.mountlogancap.com. Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8‑K, proxy statements and other information filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, are available free of charge on our investor relations website as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The SEC also maintains a website that contains our SEC filings at www.sec.gov.

We routinely announce material information to investors and the marketplace using filings with the SEC, press releases, public conference calls, presentations, webcasts, and the investor relations page of our website at ir.mountlogan.com and our LinkedIn page. We use these channels for purposes of compliance with Regulation FD and as routine channels for distribution of important information. While not all of the information that we post to the investor relations page of our website or to our LinkedIn page is of a material nature, some information could be deemed to be material. Accordingly, investors should monitor these channels, in addition to following our press releases, SEC filings, and public conference calls and webcasts. Our web addresses are included in this Annual Report on Form 10-K as textual references only and the information posted on these websites are not incorporated by reference in this Annual Report on Form 10-K or in any of our other filings with the SEC.

16

Item 1A. Risk Factors

Investing in our common stock involves a high degree of risk. The risks and uncertainties described below should be carefully considered, together with all of the other information in this Annual Report on Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, before making a decision to invest in our common stock. Our business, financial condition, results of operations, or prospects could also be harmed by risks and uncertainties not currently known to us or that we currently do not believe are material. If any of the risks actually occur, our business, financial condition, results of operations, and prospects could be adversely affected. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

Summary Risk Factors

•A portion of our revenues, earnings and cash flow is highly variable, which may make it difficult for us to achieve steady earnings growth on a quarterly basis and may cause the price of shares of our common stock to be volatile.

•We operate in highly competitive industries, which could limit our ability to achieve our growth strategies.

•We rely on technology and information systems (including those of BCPA through our Servicing Agreement with BCPA), some of which are controlled by third-party vendors, to maintain the security of our information and technology networks and to conduct our businesses.

•Our business, financial condition, results of operations, liquidity and cash flows depend on the accuracy of our management’s assumptions and estimates.

•Some of the funds ML Management manages invest in illiquid assets, and some of the investments of our insurance business are relatively illiquid.

•We rely on the financing markets for the operation of our business.

•There can be no guarantee as to the timing or amount of dividends, and shareholders may not receive dividends.

•We rely on BCPA and key BCPA personnel.

•Our relationship with BCPA will result in significant actual and potential conflicts of interest that could impact our business.

•We, through ML Management, may only manage a limited number of funds and investments.

•Our insurance business is heavily regulated and changes in regulation could reduce our profitability.

•Ability operates in a highly competitive industry that includes a number of companies, many of which are larger and more well-known, which could limit Ability’s capacity to increase or maintain market share and/or margins.

•Ability faces risks associated with business it reinsures and business it cedes to reinsurers.

•Ability is subject to regulatory capital requirements in the United States.

Risks Related to the Business – General

A portion of our revenues, earnings and cash flow is highly variable, which may make it difficult for us to achieve steady earnings growth on a quarterly basis and may cause the price of shares of our common stock to be volatile.

A portion of our revenues, earnings and cash flow is highly variable, primarily due to the nature of the insurance business of our subsidiary, Ability and the fact that fees from our Asset Management segment vary significantly from quarter to quarter and year to year. We may also experience fluctuations in our results from quarter to quarter and year to year due to a number of other factors, including changes in our operating expenses, policyholder behavior, the degree to

17

which we encounter competition and general economic and market conditions. Our future results will also be dependent on the success of the vehicles ML Management manages, changes in the value of which may result in fluctuations in our results. Such variability may lead to volatility in the trading price of shares of our common stock and cause our results for a particular period not to be indicative of our performance in a future period. It may be difficult for us to achieve steady growth in earnings and cash flow on a quarterly basis, which could in turn lead to adverse movements in the price of shares of our common stock or increased volatility in the price of shares of our common stock in general.

We operate in highly competitive industries, which could limit our ability to achieve our growth strategies and could materially and adversely affect our businesses, financial condition, results of operations, cash flows and prospects.

We operate in highly competitive markets and compete with a large number of investment management firms, private credit fund sponsors, U.S. and non-U.S. insurance and reinsurance companies and other financial institutions. In particular, our Asset Management segment faces competition in the pursuit of clients, and our insurance business faces competition with respect to both the products we offer and insurance transactions we pursue. These competitive pressures may have a material and adverse effect on our growth, business, financial condition, results of operations, cash flows and prospects.

We rely on technology and information systems (including those of BCPA through our Servicing Agreement with BCPA), some of which are controlled by third-party vendors, to maintain the security of our information and technology networks and to conduct our business, and any failures or interruptions of these systems could adversely affect our business and results of operations.

We are subject to various risks and costs associated with the collection, handling, storage and transmission of proprietary or confidential information. In the ordinary course of business, we collect and store a range of data, including our proprietary business information and intellectual property, which may include personally identifiable information relating to our insurance business or of our employees, our investors, and other third parties, in data centers and on our or BCPA’s networks, and we rely on technology and information systems in our business activities. We rely on a host of information systems and hardware systems, including those of BCPA and BCPA’s third party vendors, for the secure processing, maintenance and transmission of this information, and the unavailability of these systems or the failure of these systems to perform as anticipated for any reason could disrupt our businesses and could result in decreased performance and increased operating costs, causing our businesses and results of operations to suffer.

There can be no assurance that the various procedures and controls we utilize to mitigate the threat of cyberattacks or other similar incidents will be sufficient to prevent disruptions to our systems, especially because the cyberattack techniques used change frequently and are not recognized until launched, the full scope of a cyberattack may not be realized until an investigation has been performed and cyberattacks can originate from a wide variety of sources. Although we and BCPA take protective measures to prevent and address potential cyberattacks, there can be no assurance that any of these measures will prove effective. The rapid evolution and increasing prevalence of artificial intelligence technologies may also increase our cybersecurity risks.

We rely on BCPA and third-party service providers for certain aspects of our businesses, including for certain information systems and technology. We cannot guarantee that BCPA, third party vendors, service providers and lenders have not been compromised or that they do not contain exploitable defects or bugs that could result in a breach of or disruption to our information technology systems or the BCPA or third-party information technology systems that support our business. Our ability to monitor these third parties’ information security practices is limited, and they may not have adequate information security measures in place. In addition, if BCPA or one of our third-party counterparties suffers a security breach, our response may be limited or more difficult because it may not have direct access to their systems. A disaster, disruption or compromise in technology or infrastructure that supports our businesses, including a disruption involving electronic communications or other services used by us, may have an adverse impact on our ability to continue to operate our businesses without interruption, which could have a material adverse effect on us. These risks could increase due to the increasing use of cloud-based software services. In addition, costs related to data security threats or disruptions may not be fully insured or indemnified by other means.

As new technologies, including tools that harness generative artificial intelligence and other machine learning techniques, rapidly develop and become even more accessible, the use of such new technologies by us, our affiliates and our third party service providers and other vendors will present additional known and unknown risks, including, among others, the risk that confidential information may be stolen, misappropriated or disclosed and the risk that we and/or our third party service providers or other vendors may rely on incorrect, unclear or biased outputs generated by such technologies, any of which could have an adverse impact on us and our business.

18

A significant actual or potential theft, loss, corruption, exposure, fraudulent, unauthorized or accidental use or misuse of personally identifiable or proprietary business data could result in significant remediation and other costs, fines, litigation and regulatory actions against us, in addition to significant reputational harm.

Our business, financial condition, results of operations, liquidity and cash flows will depend on the accuracy of our management’s assumptions and estimates, and we could experience significant gains or losses if these assumptions and estimates differ significantly from actual results.

We make and rely on certain assumptions and estimates regarding many matters related to our businesses, including interest rates, expenses and operating costs, tax assets and liabilities, tax rates, business mix, and contingent liabilities. We also use these assumptions and estimates to make decisions crucial to our business operations. The factors influencing these various assumptions and estimates cannot be calculated or predicted with certainty, and if our assumptions and estimates differ significantly from actual outcomes and results, our business, financial condition, results of operations, liquidity and cash flows may be materially and adversely affected.

Some of the funds ML Management manages invest in illiquid assets, and some of the investments of our insurance business are relatively illiquid. Funds holding such assets and we, as applicable, may fail to realize profits from these assets for a considerable period of time, or lose some or all of the amount that is invested in these assets if such assets are required to be sold at inopportune times or in response to changes in applicable rules and regulations.

Some of the funds ML Management manages invest in securities or other financial instruments that are not publicly traded or are otherwise viewed as “illiquid.” In such cases, there may be limitations by contract or by applicable securities laws on the sale of such securities or financial instruments, such that they can only be sold after a period of time and then only at such times when we will not possess material nonpublic information. In addition, the ability to dispose of private credit investments prior to maturity is generally heavily dependent upon the secondary trading market for such instruments. Such markets may not be available. Accordingly, the funds ML Management manages may be forced, under certain conditions, to sell securities at a loss.

In addition, some investments by Ability, our insurance business, are in securities that are not publicly traded or that otherwise lack liquidity. These relatively illiquid types of investments are recorded at fair value. If a material liquidity demand is triggered and our insurance business is unable to satisfy the demand with the sources of liquidity available to it, our insurance business could be forced to sell certain of its assets and there can be no assurance that it would be able to sell them for the values at which such assets are recorded and it might be forced to sell them at significantly lower prices. In some cases, our insurance business may also be prohibited by contract or applicable securities laws from selling such securities for a period of time. Thus, it may be impossible or costly to liquidate positions rapidly in order to meet unexpected obligations. This potential mismatch between the liquidity of assets and liabilities could have a material and adverse effect on our business, financial condition, results of operations and cash flows.

Further, governmental and regulatory authorities periodically review legislative and regulatory initiatives, and may promulgate new or revised, or adopt changes in the interpretation and enforcement of existing, rules and regulations at any time that may impact our investments. Such changes in regulatory requirements could disrupt market liquidity, make it more difficult for us to operate our business, and cause securities that are not publicly traded to lose value, any of which could have a material and adverse effect on our business, financial condition or results of operations.

We rely on the financing markets for the operation of our business.

We rely on the debt and equity financing markets for the operation of our business. To the extent that debt and equity markets render financing difficult to obtain, refinance or extend, or more expensive, this may have a material and adverse effect on our business, financial condition, results of operations, liquidity and cash flows.

In particular, our insurance business relies on access to lending and debt markets to provide capital and liquidity. Changes in debt financing markets may impact our insurance business’s access to capital and liquidity. Calculations of required insurance capital may move with market movements and result in greater capital needs during economic downturns. Our insurance business may also need additional liquidity to pay insurance liabilities in excess of its assumptions.

The absence of available sources of debt financing for extended periods of time could materially and adversely affect us. In the event that we are unable to obtain debt financing, or can only obtain debt at an increased interest rate or otherwise on unfavorable terms, we may be forced to find alternative sources of financing (including equity), may have difficulty executing our business objectives or may generate profits that are lower than would otherwise be the case, any of which could lead to a decrease in the income earned by us. If we use leverage in the future, shareholders should be aware that investments in leveraged entities are inherently more sensitive to declines in revenues, increases in expenses and

19

interest rates and adverse economic, market and industry developments. As a result, the risk of loss associated with a leveraged entity is generally greater than for companies with comparatively less debt.

We, and particularly our insurance business, may acquire various financial instruments for purposes of “hedging” or reducing its risks, which may be costly and ineffective and could reduce its cash available for distribution to its shareholders.