S-1: General form for registration of securities under the Securities Act of 1933

Published on January 12, 2026

As filed with the Securities and Exchange Commission on January 12, 2026

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of Registrant as specified in its charter)

Delaware | 6282 | 33-2698952 | ||||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) | ||||||

650 Madison Avenue, 3rd Floor

New York, New York 10022

(212) 891-2880

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Nikita Klassen | ||

Chief Financial Officer and Corporate Secretary | ||

Mount Logan Capital Inc. | ||

650 Madison Avenue, 3rd Floor | ||

New York, NY 10022 | ||

212-891-2880 | ||

(Name, address, including zip code, and telephone number, including area code, of agent for service)

with a copy to:

Kenneth E. Young, Esq. | ||

Stephen R. Pratt, Esq. | ||

Anna Tomczyk, Esq. | ||

Dechert LLP | ||

3 Bryant Park | ||

| 1095 Avenue of the Americas | ||

| New York, NY 10036 | ||

212-698-3500 | ||

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

THE INFORMATION IN THIS PRELIMINARY PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PRELIMINARY PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

Subject to Completion, dated January 12, 2026

PRELIMINARY PROSPECTUS

Mount Logan Capital Inc.

$40,000,000

% Notes Due 2031

Mount Logan Capital Inc. (f/k/a Yukon New Parent, Inc.) (“Mount Logan”, “we” or “us”) (Nasdaq: MLCI) is a diversified alternative asset management and insurance solutions platform. Our mission is to provide our investors with access to a diversified and differentiated set of private market investment solutions to address their capital needs. We conduct our business primarily in the United States through our two business segments: Asset Management and Insurance Solutions. Mount Logan Management LLC (“ML Management”), our Securities and Exchange Commission-registered investment adviser, manages a significant portion of our assets under management (“AUM”) across its various managed funds supported by permanent and semi-permanent capital bases. We tailor our asset management platform to serve high-growth client segments within the institutional, retail, and insurance markets. ML Management also directly manages the capital of our wholly-owned insurance company, Ability Insurance Company (“Ability”), for the benefit of policyholders. Ability, a Nebraska domiciled insurer, specializes in reinsuring annuity products for the increasing number of individuals seeking to fund retirement needs and represents all of our insurance solutions operations.

We are offering $40,000,000 in aggregate principal amount of our % Notes due 2031 (the “Notes”). The Notes will mature on . We will pay interest on the Notes quarterly in arrears on and of each year, beginning , 2026. The purchase price of the Notes includes accrued interest on the Notes from , 2026 to, but not including, the date of delivery. We may redeem the Notes in whole or in part at any time or from time to time on or after at the redemption price of 100% of aggregate principal amount, plus any accrued and unpaid interest, as discussed under “The Offering — Optional Redemption” and “Description of Notes — Optional Redemption” in this prospectus. The Notes will be issued in minimum denominations of $25 and integral multiples of $25 in excess thereof.

The Notes will be our direct senior unsecured obligations and rank pari passu with all outstanding and future unsecured unsubordinated indebtedness issued by Mount Logan.

We intend to apply to list the Notes on The Nasdaq Global Market under the trading symbol “MLCIL,” and if the application is approved, we expect trading in the Notes on The Nasdaq Global Market to begin within 30 days of the original issue date. The Notes are expected to trade “flat,” which means that purchasers will not pay, and sellers will not receive, any accrued and unpaid interest on the Notes that is not included in the trading price. Currently, there is no public market for the Notes.

We are an “emerging growth company” and a “smaller reporting company” under applicable federal securities laws and will be subject to reduced public company reporting requirements. Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 15 to read about factors you should consider, including the risk of leverage, before investing in our securities.

This prospectus contains important information you should know before investing in our securities. Please read it before you invest and keep it for future reference.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Note | Total | ||||||||||

Public Offering Price(1) | $ | $ | |||||||||

Underwriting Discounts and Commissions | $ | $ | |||||||||

Proceeds to Mount Logan, before expenses(2) | $ | $ | |||||||||

_______________

(1)Plus accrued interest, if any, from , 2026, if settlement occurs after that date.

(2)Before deducting expenses payable by us related to the offering, estimated at $ . See “Underwriting (Conflicts of Interest)” in this prospectus.

The underwriters may also purchase up to an additional $6,000,000 aggregate principal amount of Notes offered hereby, to cover over-allotments, if any, within 30 days of the date of this prospectus. If the underwriters exercise this option in full, the total public offering price will be $ , the total underwriting discount and commissions paid by us will be $ , and total proceeds to us, before expenses, will be $ .

We may increase the aggregate principal amount of Notes offered in this offering (inclusive of any additional aggregate principal amount of Notes subject to the underwriters’ over-allotment option) by up to an additional $35.0 million, depending on market conditions and investor demand. Any such increase will be within the maximum aggregate offering price of securities registered under the registration statement of which this prospectus forms a part.

Delivery of the Notes in book-entry form only through The Depository Trust Company (“DTC”) and its participants, including Clearstream Banking, société anonyme (“Clearstream”) and Euroclear Bank SA/NV, as operator of the Euroclear system (“Euroclear”), will be made on or about , 2026.

Joint Book-Running Managers

Lucid Capital Markets | Piper Sandler | BC Partners Securities | ||||||

Co-Managers

Canaccord Genuity | William Blair | Wedbush Securities | ||||||

The date of this prospectus is , 2026

TABLE OF CONTENTS

Page | |||||

You should rely only on the information contained in this prospectus, any free writing prospectus prepared by us or information to which we have referred you. We have not authorized any agent, dealer, salesman or other person to give any information or to make any representation other than those contained in this prospectus. You must not rely upon any information or representation not contained in this prospectus. This prospectus does not constitute an offer to sell or a solicitation of any offer to buy any security other than the registered securities to which this relates, nor does it constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in such jurisdiction. The information contained in this prospectus is accurate as of the date on its cover. Our business, financial condition, results of operations and prospects may have changed since then.

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements in this prospectus constitute forward-looking statements which relate to future events or our future performance or financial condition. In some cases, you can identify these forward-looking statements by the use of words such as “outlook,” “believes,” “expects,” “potential,” “may,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated.

See “Risk Factors” beginning on page 15 to read about factors you should consider, including the risk of leverage, before investing in our securities. Forward-looking statements speak as of the date on which they are made, and we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law. We have based the forward-looking statements included in this prospectus on information available to us on the date of this prospectus, and we assume no obligation to update any such forward-looking statements. Actual results could differ materially from those anticipated in our forward-looking statements, and future results could differ materially from historical performance.

You should understand that, under Sections 27A(b)(2)(B) of the Securities Act and Section 21E(b)(2)B of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 do not apply to statements made in connection with any offering of securities pursuant to this prospectus or in any report that we file under the Exchange Act.

1

CERTAIN DEFINED TERMS

When used in this document, unless otherwise indicated in this document or the context otherwise requires:

•“180 Degree Capital” refers to 180 Degree Capital Corp., a corporation organized under the Laws of the State of New York;

•“1940 Act” refers to the Investment Company Act of 1940, as amended;

•“Advisers Act” refers to the Investment Advisers Act of 1940, as amended;

•“AUM” refers to assets under management;

•“BC Partners” refers to BC Partners LLP, an adviser of private equity and real estate funds affiliated with BCPA;

•“BC Partners PE/RE Affiliates” refers to affiliates of BC Partners involved in the private equity and real estate business, and for the avoidance of doubt, does not include BCPA or the BCPA Credit Affiliates;

•“BCPA” refers to BC Partners Advisors L.P., an adviser of credit funds affiliated with BC Partners;

•“BCPA Credit Affiliates” refers to affiliates of BCPA involved in the credit business, and for the avoidance of doubt, does not include BC Partners or the BC Partners PE/RE Affiliates;

•“Board” refers to the Board of Directors of Mount Logan;

•“Business Combination” refers to the combination of the businesses of 180 Degree Capital and Mount Logan and any other transactions contemplated by and pursuant to the terms of the Merger Agreement;

•“Credit Facility” or “Credit Agreement” refers to the Credit Agreement, dated as of August 20, 2021 (as amended from time to time), by and between MLC US Holdings LLC and a large US-based asset manager, as administrative agent and collateral agent for the lenders;

•“Legacy MLC” refers to Mount Logan Capital Inc., a corporation organized under the laws of the Province of Ontario;

•“Merger Agreement” refers to the agreement and plan of merger, dated January 16, 2025, as amended on July 6, 2025, by the Merger Agreement Amendment, among 180 Degree Capital, Mount Logan, Legacy MLC, Polar Merger Sub, Inc., and Moose Merger Sub, LLC, as it may from time to time be further amended, modified or supplemented;

•“MLC Merger Sub” refers to Moose Merger Sub, LLC, a limited liability company formed under the Laws of the State of Delaware;

•“Nasdaq” refers to The Nasdaq Capital Market;

•“Nasdaq Listing Rules” refers to the rules and listing standards of Nasdaq;

•“NAV” refers to net asset value;

•“SEC” refers to the U.S. Securities and Exchange Commission;

•“Securities Act” refers to the United States Securities Act of 1933, as amended;

•“Subsidiary,” when used with respect to any Person, refers to any corporation, partnership, limited liability company or other Person, whether incorporated or unincorporated, that is consolidated with such Person for financial reporting purposes under generally accepted accounting principles; and

2

•“TURN Merger Sub” refers to Polar Merger Sub, Inc., a corporation organized under the Laws of the State of New York.

3

AVAILABLE INFORMATION

This prospectus is part of a registration statement on Form S-1 we have filed with the SEC under the Securities Act to register the securities offered by this prospectus. The registration statement of which this prospectus is a part contains additional information about us and this offering.

We file annual, quarterly and current reports, and other information with the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements and other information that we file electronically with the SEC at www.sec.gov, from which interested persons can electronically access our filings with the SEC, including the registration statement of which this prospectus is a part, including the exhibits and schedules thereto. The reports and other information we file with the SEC also are available through our website at https://ir.mountlogan.com. Information on our website is not incorporated into or a part of this prospectus, other than documents that we file with the SEC that are incorporated by reference in this prospectus.

You may also request a copy of any of our filings with the SEC orally or in writing, at no cost to the requester, directed to the following address: 650 Madison Avenue, 3rd Floor, New York, New York 10022.

No person is authorized by us to give any information or to make any representations other than those contained or incorporated by reference in this prospectus, and, if given or made, such information or representations must not be relied upon as having been authorized by us. Neither the delivery of this prospectus nor any distribution of securities made hereunder shall imply that there has been no change in the information set forth herein or in our affairs since the date hereof.

4

PROSPECTUS SUMMARY

This summary highlights some of the information in this prospectus. It is not complete and does not contain all of the information that you should consider before investing in the notes. You should carefully read the entire prospectus, including the section entitled “Risk Factors,” along with the financial data and related notes and other information included in this prospectus.

As used in this Prospectus, unless otherwise indicated or the context otherwise requires, references to “we,” “us,” “our,” the “Company,” and “Mount Logan” refer to the consolidated operations of Mount Logan Capital Inc. (fka Yukon New Parent, Inc.) and its wholly owned subsidiaries following the Business Combination. References to “Legacy MLC” refer to Mount Logan Capital Inc., a corporation organized under the laws of the Province of Ontario, prior to the consummation of the Business Combination and references to “180 Degree Capital” refer to 180 Degree Capital Corp., a corporation organized under the Laws of the State of New York, prior to the consummation of the Business Combination.

Overview of Mount Logan Capital Inc.

Formed in 2018, Mount Logan is a publicly traded, alternative asset management and insurance solutions platform. Our mission is to provide investors in our funds, accounts and other vehicles access to a diversified and differentiated set of private market investment solutions to address their capital needs and generate attractive risk-adjusted returns on their behalf. We conduct our business primarily in the United States through our two business segments: Asset Management and Insurance Solutions. ML Management, our wholly-owned, SEC-registered investment adviser, manages a significant portion of our AUM across its various managed funds supported by permanent and semi-permanent capital bases. We tailor our asset management platform to serve high-growth client segments within the institutional, retail, and insurance markets.

Ability is a Nebraska domiciled insurer and reinsurer, specializing in reinsuring annuity products for the increasing number of individuals seeking to fund retirement needs and represents all of our insurance solutions operations. Today Ability is the primary business that comprises our Insurance Solutions segment. ML Management manages a significant portion of Ability’s investment portfolio under guidelines designed to support policyholder obligations while generating durable Spread Related Earnings (“SRE”), a key financial metric that we define and report as a non-GAAP financial measure.

5

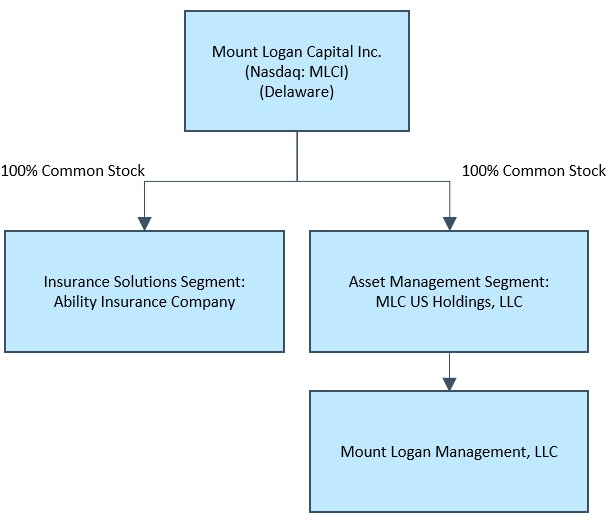

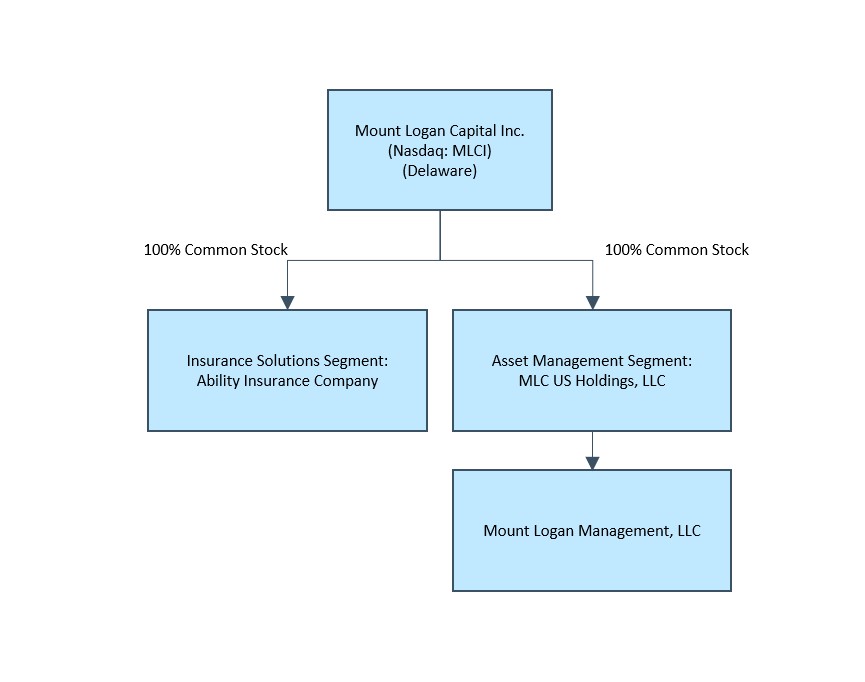

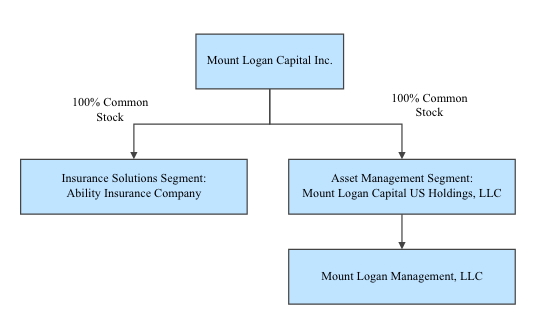

The diagram below depicts our current organizational structure:

Note: The organizational structure chart above depicts a simplified version of the Mount Logan structure. It does not include all legal entities in the structure. The acquisition of 180 Degree Capital Corp. is reflected as part of the Asset Management segment.

Business Strategy

Asset Management

Our Asset Management segment focuses on private credit across senior secured lending, asset-based and specialty finance, structured and opportunistic credit, venture and growth lending, and select equity-linked solutions. We provide origination, underwriting, portfolio construction and risk management to a diversified client base, including insurance accounts, a BDC platform, our interval funds (SOFIX, ACIF), Separately Managed Accounts (“SMAs”) and other vehicles. We manage substantially all of the assets of Ability, our primary Insurance Solutions business, and maintain an active dialogue with the insurance solutions team.

For these services, we generate recurring fee streams across a diversified set of credit investing strategies. After stripping out the expenses required to generate our fee revenues, the remaining profit stream constitutes Fee Related Earnings (“FRE”), our primary performance measurement for this segment.

Our investment philosophy is centered around deploying capital into well-established middle-market businesses that operate across a wide range of industries, while limiting concentration in any one industry. We employ fundamental credit analysis, targeting investments in businesses with relatively low levels of cyclicality and operating risk. We seek to provide a full credit cycle investment offering, with the ability to opportunistically allocate capital to fill the white space created as other capital sources retrench. As part of our opportunistic allocation of capital, we are able to underwrite complex, less competitive niches, and deploy capital during periods of uncertainty with a consistent emphasis on downside protection and preservation of capital. Many of our mandates utilize multi-year, permanent or semi-permanent capital, allowing us to invest patiently across the capital structure,

6

scale AUM, and compound recurring FRE through cycles. As of September 30, 2025, we had total AUM in excess of $2.1 billion.

We have experience managing levered vehicles, both public and private, and seek to enhance returns through the prudent use of leverage with a conservative approach that prioritizes downside protection and capital preservation. We believe this strategy and approach offers attractive risk-adjusted returns with lower volatility given the potential for fewer defaults and greater resilience through market cycles.

Permanent or Semi-Permanent Capital

Included within our investing strategies above is $1.4 billion of permanent or semi-permanent capital, out of the over $2.1 billion of total AUM, as of September 30, 2025. As of September 30, 2025, permanent capital includes, without limitation, certain assets in our credit strategy, including assets relating to publicly traded and non-traded vehicles, and assets managed for certain of our Insurance Solutions clients, which have indefinite or long-term investment horizons, and in specific cases provide stable sources of funding while allowing for liquidity access for investors through redemption mechanisms. We do not include vehicles with definite term, finite investment periods, or funds that are in wind-down in our definition and aggregation of permanent or semi-permanent capital.

Insurance Solutions

Our retirement-style spread model centers on two core competencies: (i) sourcing long-duration, persistent liabilities via reinsurance treaties, and (ii) deploying those premiums into diversified investment grade and private credit portfolios, constructed and risk-managed by ML Management. We prioritize asset-liability management and capital stewardship, seeking incremental yield primarily by underwriting complexity and liquidity where we believe we are compensated at an attractive risk adjusted return rather than by assuming outsized credit risk. Post-Business Combination, we expect that our stronger balance sheet will enhance our capacity to scale reinsurance production, broaden product offerings over time, and support policyholder stability.

Our Insurance Solutions investment program is designed to earn incremental yield by taking measured liquidity and complexity risk commensurate with long-dated liabilities, while relying on ML Management’s origination and underwriting discipline. We measure performance using SRE, which captures net investment earnings after cost of funds and operating expenses.

Integrated Model and Financial Flexibility

Our Asset Management and Insurance Solutions businesses are strategically integrated: ML Management sources and allocates assets with asset-liability management discipline for Ability. Ability’s liabilities and spread income reinforce the durability of our fee and spread earnings. Following the combination with 180 Degree Capital, we expect increased access to capital and a strengthened balance sheet to accelerate both organic initiatives (such as new strategies, fund scaling, and reinsurance flow) and targeted inorganic growth, further supported by ongoing servicing and scale provided from BCPA. The strength of our platform is built on the experience of our leadership team, the capabilities of a world-class investment team, and strong operational support.

Growth Strategy

We are building a diversified alternative asset management and insurance solutions platform. With the completion of the 180 Degree Capital transaction and our Nasdaq listing, we believe we have improved access to the capital markets, improved financing flexibility and a stronger balance sheet to accelerate organic and inorganic growth initiatives. Our team’s priorities include (i) investing into Ability to support increased reinsurance flows to expand Ability’s liabilities and investment portfolio to generate positive SRE, primarily managed by our registered advisor, Mount Logan Management LLC; (ii) scaling our private credit AUM across existing and future vehicles to increase FRE; and (iii) selective acquisitions and partnerships that broaden origination, diversify products, and enhance operating leverage. These initiatives are intended to reinforce shareholder value by compounding FRE and SRE via a capital flywheel. As assets under management increase, FRE rises, generating additional cash flow at the parent company. We can reinvest this cash into Ability to support new reinsurance treaties, which expand liabilities and invested assets. These assets generate SRE while also increasing AUM managed by Mount Logan, which in turn

7

produces more FRE and cash flow to be re-deployed. We pursue this growth within a framework of disciplined underwriting, regulatory compliance, and capital management.

Asset Management

Our objective is to become a fully diversified private credit manager for institutional, retail and insurance clients. We are growing AUM in existing vehicles, new strategies, and through accretive acquisitions and partnerships that add capital and incremental origination channels. We intend to: (i) expand AUM in our existing vehicles; (ii) launch adjacent strategies that can scale through our distribution network; and (iii) pursue acquisitions or partnerships that add origination and recurring fees. These initiatives are supported by our permanent and semi-permanent capital base and our track record managing diverse investment vehicles. We are capitalizing on secular tailwinds as banks continue to re-trench and private credit fills the gap. We evaluate new vehicle launches, acquisitions and partnerships based on a number of factors including: (i) strategic fit (e.g. credit capability expansion, distribution); (ii) durability of capital (i.e. permanent or semi-permanent capital, what we refer to as "sticky AUM"); (iii) underwriting culture, risk controls, and unit economics (e.g., FRE uplift and margin accretion); and (iv) ease of integration into our operating model, as supported by our Staffing and Resource Agreement and Servicing Agreement (each as defined below) with BCPA.

Insurance Solutions

We are scaling a capital-efficient insurance platform pairing long-dated, predictable liabilities with our private credit origination and underwriting capabilities. A strengthened balance sheet following our combination with 180 Degree Capital positions us to grow our insurance capabilities. Our objectives include:

Expand Multi-Year Guaranteed Annuity (“MYGA”) Reinsurance Through Diversified Channels: Our insurance solutions segment, through Ability, is initially focused on MYGA reinsurance, a product with fixed tenors, high predictability, and strong growth in the fixed annuity market. We intend to increase our cadence of quota-share flow treaties and opportunistic blocks with a broader set of counterparties, building on previously executed agreements. Any new reinsurance treaties we enter into will be filed with and approved by appropriate state insurance regulatory authorities before being executed.

Increase our Risk Based Capital (“RBC”) Ratios via Direct Investments from Mount Logan, compounding SRE and Reinforcing the Asset Management “Flywheel”: Mount Logan as Parent can invest capital directly into Ability to support MYGA reinsurance and other insurance activities that we may pursue in the future. Through our asset management segment, we target attractive spread economics and active portfolio management to optimize Ability’s assets, while earning a management fee for performing these activities. The flywheel between asset management and insurance solutions is a key driver of the compounding growth of our business.

Broaden Product Set and Strengthen Distribution: Over time we plan to expand beyond MYGA into additional retirement and life protection solutions, including fixed indexed annuities and pre-need products, subject to market conditions and required regulatory approvals. We also plan to diversify distribution by adding new counterparties and pursuing block transactions. Over time, we may evaluate direct-writing opportunities to complement reinsurance channels. As scale increases across products and channels, we expect improved operating leverage, more durable SRE, and continued discipline around asset-liability management, RBC ratios, and regulatory capital.

Legacy MLC

Historically, our predecessor, Legacy MLC, focused on strategic acquisitions and partnerships to expand its asset management capabilities, including but not limited to (i) the 2020 transaction alongside Sierra Crest Investment Management (“SCIM”), whereby SCIM became the investment advisor to the Alternative Credit Income Fund (“ACIF”), (ii) the purchase of, and subsequent increase in, a minority stake in SCIM, which manages BCP Investment Corporation (“BCIC”), formerly Portman Ridge Finance Corp. (“Portman Ridge”), a closed-end, externally managed, non-diversified investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, (iii) the 2021 acquisition of certain assets from Capitala Investment Advisors, LLC, whereby ML Management became the manager of Logan Ridge Finance Corp.

8

(formerly Capitala Finance Corp.), also a BDC, which has since merged with and into Portman Ridge (see “— Recent Developments — The Portman-Logan Merger”), and (iv) the transaction with Ovation Partners, LP, for the management of its alternative income platform, which included the transfer of employees to ML Management to support its specialty finance and asset-backed finance efforts across commercial lending, real estate lending, consumer finance, and litigation finance.

The Asset Management segment also holds a minority equity interest in Runway Growth Capital, LLC (“Runway”), which is a private credit, SEC-registered investment adviser managing in excess of $1.1 billion AUM (as of September 30, 2025) with a specific orientation on providing growth capital to sponsored (i.e., venture-backed) and non-sponsored companies that are looking for an alternative to raising equity capital. The minority investment in Runway Growth Capital was acquired during the first quarter of 2025 by Legacy MLC, but for purposes of this filing is not considered a significant investment in accordance with Rule 3-09 of Regulation S-X.

Recent Developments

The Merger

On September 12, 2025, we completed the previously announced Business Combination through two simultaneous merger transactions pursuant to the Agreement and Plan of Merger. In the first merger, TURN Merger Sub merged with and into 180 Degree Capital, with 180 Degree Capital surviving as our wholly-owned subsidiary. In the second merger, MLC Merger Sub merged with and into Legacy MLC, with Legacy MLC surviving as our wholly-owned subsidiary.

Following the completion of these merger transactions, we changed our name from “Yukon New Parent, Inc.” to “Mount Logan Capital Inc.” and became a publicly traded corporation.

The Portman-Logan Merger

On January 30, 2025, the Company announced that it had completed its previously announced minority investment in Runway, alongside BCPA and its affiliates, which acquired the remaining outstanding ownership in Runway.

On January 30, 2025, Portman Ridge and Logan Ridge announced that they had entered into an agreement under which Logan Ridge would merge with and into Portman Ridge (the “Portman-Logan Merger”), subject to the receipt of certain shareholder approvals and the satisfaction of other closing conditions, including a payment by ML Management of approximately $1.25 million to the former shareholders of Logan Ridge in July 2025.

On July 15, 2025, Portman Ridge announced the closing of the Portman-Logan Merger. The Company, through ML Management, previously acquired an investment management agreement (“IMA”) through an asset purchase that resulted in ML Management becoming the investment advisor of Logan Ridge. The merging of Logan Ridge into Portman Ridge resulted in Logan Ridge’s existing IMA being terminated and, therefore, the Company's management fee stream from Logan Ridge ceasing. Portman Ridge was subsequently renamed to BCP Investment Corporation (“BCIC”). In connection with the closing of the Portman-Logan Merger, MLCSC Holdings LLC, our wholly-owned subsidiary (“MLCSC”), entered into a profit-sharing agreement with BCPSC Holdings LLC, pursuant to which MLCSC received economic interests in units worth 16.03% of BCPA’s distributions received under SCIM’s IMA with BCIC.

Tender Offer

On December 29, 2025, we issued a press release announcing that we are commencing a cash tender offer to purchase up to $15 million in value, or approximately 1,590,600 shares, of our Common Stock at a price of $9.43 per share.

Corporate Information

Mount Logan Capital Inc., the issuer of the Notes in this offering, was incorporated in Delaware on January 7, 2025. Our principal executive offices are located at 650 Madison Avenue, 3rd Floor New York, New York 10022.

9

Our telephone number is (212) 891-2880. Our corporate website is www.mountlogancap.com and ir.mountlogan.com. The information contained on or that can be accessed through our website is not incorporated by reference into this prospectus, and you should not consider information on our website to be part of this prospectus or in deciding whether to purchase the Notes.

Summary Risk Factors

Risks Relating to the Notes

•The Notes will be structurally subordinated to the indebtedness and other liabilities of our future subsidiaries, if any.

•Our amount of debt outstanding will increase as a result of this offering. Our future indebtedness could adversely affect our business, financial condition, results of operations, and ability to meet our payment obligations under the Notes and our other debt.

•We may choose to redeem the Notes when prevailing interest rates are relatively low.

•An increase in market interest rates could result in a decrease in the market value of the Notes.

•The Notes will be unsecured and therefore will be effectively subordinated to our existing secured indebtedness we may incur in the future.

•The indenture under which the Notes will be issued contains limited protection for holders of the Notes.

•Servicing our indebtedness will require a significant amount of cash. Our ability to generate sufficient cash depends on many factors, some of which are not within our control.

•We may not be able to repurchase all of the Notes upon a Change of Control (as defined below).

•There is currently no market for the Notes, and we cannot assure you that an active trading market for the Notes will develop. The Notes may trade at prices below the price you paid for them.

•If we default on our obligations to pay our other indebtedness, we may not be able to make payments on the Notes.

•A downgrade, suspension or withdrawal of the credit rating assigned by a rating agency to us or the Notes, if any, or change in the debt markets could cause the liquidity or market value of the Notes to decline significantly.

Risks Relating to Our Business - General

•A portion of our revenues, earnings and cash flow is highly variable, which may make it difficult for it to achieve steady earnings growth on a quarterly basis and may cause the price of shares of our Common Stock to be volatile.

•We operate in highly competitive industries, which could limit our ability to achieve its growth strategies.

•We rely on technology and information systems (including those of BCPA through our Servicing Agreement (as defined and described below) with BCPA), some of which are controlled by third-party vendors, to maintain the security of our information and technology networks and to conduct our businesses.

•Our business, financial condition, results of operations, liquidity and cash flows depend on the accuracy of our management’s assumptions and estimates.

•Some of the funds ML Management manages invest in illiquid assets, and some of the investments of our insurance business are relatively illiquid.

10

•We rely on the financing markets for the operation of our business.

•There can be no guarantee as to the timing or amount of dividends, and shareholders may not receive dividends.

•We rely on BCPA and Key BCPA Personnel.

•Our relationship with BCPA will result in significant actual and potential conflicts of interest that could impact New Mount Logan’s business.

•We, through ML Management, may only manage a limited number of funds and investments.

•Our insurance business is heavily regulated and changes in regulation could reduce our profitability.

•Ability operates in a highly competitive industry that includes a number of companies, many of which are larger and more well-known, which could limit Ability’s capacity to increase or maintain market share and/or margins.

•Ability faces risks associated with business it reinsures and business it cedes to reinsurers.

•Ability is subject to regulatory capital requirements in the United States.

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We will cease to be an emerging growth company upon the earliest of: (1) the end of the fiscal year following the fifth anniversary of an initial public offering of our common equity; (2) the first fiscal year after our annual gross revenues are $1.07 billion or more; (3) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt securities; or (4) the end of any fiscal year in which the aggregate worldwide market value of the voting and non-voting common equity held by non-affiliates (or public float) exceeded $700 million as of the end of the second quarter of that fiscal year. We have taken advantage of reduced disclosure regarding executive compensation arrangements in this prospectus, and we may choose to take advantage of some but not all of these reduced disclosure obligations in future filings. If we do, the information that we provide investors may be different than the information you might get from other public companies.

The JOBS Act permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period under the JOBS Act is irrevocable.

We also qualify as a “smaller reporting company”, as defined in Rule 405 under the Securities Act. We will continue to be a smaller reporting company so long as either (i) the market value of our securities held by non-affiliates is less than $250 million as of the last business day of our most recently completed second fiscal quarter, or (ii) our annual revenue was less than $100 million during our most recently completed fiscal year and the market value of the shares of our Common Stock held by non-affiliates is less than $700 million as of the last business day of our most recently completed second fiscal quarter. If we continue to qualify as a smaller reporting company at the time we cease to be an emerging growth company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. In particular, for so long as we remain a smaller reporting company, we (i) may choose to present only the two most recent fiscal years of audited financial

11

statements in our Annual Report on Form 10-K, and (ii) have reduced disclosure obligations regarding executive compensation.

12

SUMMARY OF THE OFFERING

Issuer | Mount Logan Capital Inc. | |||||||

Notes Offered | $40,000,000 aggregate principal amount of % Notes due 2031 (the “Notes”). | |||||||

Option to Purchase Additional Notes | The underwriters may also purchase from us up to an additional $6,000,000 aggregate principal amount of Notes within 30 days of the date of this prospectus. | |||||||

Offering Price | % of the aggregate principal amount, or $ per Note. The purchase price of the Notes includes accrued interest on the Notes from , 2026 to, but not including, the date of delivery. | |||||||

Maturity Date | The Notes will mature on , 20 . | |||||||

Interest Rate and Payment Dates | Interest of % per annum on the principal amount of the Notes will be payable in arrears on and of each year, commencing on , 2026. Interest will accrue on the Notes from , 2026. | |||||||

Ranking | The Notes will be our senior unsecured obligations and will rank senior in right of payment to all of our obligations that are expressly subordinated in right of payment to the Notes and equally in right of payment with all of our existing and future senior unsecured indebtedness. In addition, the Notes will effectively rank junior in right of payment to any of our existing and future secured indebtedness to the extent of the value of the assets securing such indebtedness. As of September 30, 2025, we had $38.0 million of secured indebtedness that would have effectively ranked senior in right of payment to the Notes, $36.3 million of unsecured indebtedness that would have effectively ranked senior in right of payment with the Notes, no indebtedness that would have ranked equally in right of payment with the Notes, and no subordinated indebtedness that would have ranked junior in right of payment to the Notes. All of our indebtedness at such date was indebtedness of our subsidiaries and was scheduled to mature after the expected maturity date of the Notes. See “Description of Other Indebtedness” for a detailed description of our indebtedness. | |||||||

Covenants | The indenture (as defined below) contains various covenants by which the Company and its subsidiaries will be bound. See “Description of Notes— Covenants.” | |||||||

Optional Redemption | Except as described under “Description of Notes—Optional Redemption Upon Change of Control,” the Notes may not be redeemed by us, at our option, prior to (the “Par Call Date”). We may redeem the Notes, in whole or in part, at any time and from time to time on and after the Par Call Date at a redemption price equal to 100% of the principal amount of the Notes being redeemed plus accrued and unpaid interest thereon to, but excluding, the redemption date. See “Description of Notes—Optional Redemption.” | |||||||

Optional Redemption Upon Change of Control | If a Change of Control with respect to the Notes occurs, the Notes may be redeemed for cash in whole but not in part at our option at any time within 90 days of the occurrence of a Change of Control, at a repurchase price equal to 100% of the principal amount of the Notes to be repurchased, plus accrued and unpaid interest thereon to, but excluding, the date of redemption. See “Description of Notes—Optional Redemption Upon Change of Control.” | |||||||

13

Use of Proceeds | We estimate that the net proceeds from the sale of the Notes in this offering will be approximately $ (or approximately $ if the underwriters fully exercise their overallotment option), after deducting the underwriting discount and estimated offering expenses payable by us. We anticipate using the net proceeds from the sale of the Notes to repay outstanding indebtedness under the Credit Facility and any remainder for general corporate purposes. See “Use of Proceeds.” | |||||||

Further Issuances | We may issue additional Notes having the same terms, with certain exceptions, as the Notes offered hereby; provided that if the additional Notes are not fungible with the original Notes offered hereby for U.S. federal income tax purposes, the additional Notes will have a separate CUSIP number so that they are distinguishable from the Notes offered hereby. | |||||||

Absence of Public Market for the Notes | The Notes are a new issue of securities, and there is currently no established trading market for the Notes. We intend to apply to list the Notes on The Nasdaq Global Market under the symbol “MLCIL,” and if the application is approved, we expect trading in the Notes on The Nasdaq Global Market to begin within 30 days of the original issue date. The Notes are expected to trade “flat,” which means that purchasers will not pay, and sellers will not receive, any accrued and unpaid interest on the Notes that is not reflected in the trading price. | |||||||

Indenture | The Notes will be issued under an indenture, dated as of , 2026, among the Company and U.S. Bank National Association, as trustee, to be amended and supplemented by a supplemental indenture thereto establishing the terms of the Notes to be dated as of the issue date of the Notes (collectively, the “indenture”). | |||||||

Clearance and Settlement | The Notes will be issued in book-entry form through the facilities of DTC for the accounts of its participants, including Clearstream and Euroclear, and will trade in DTC’s same day funds settlement system. Beneficial interests in Notes held in book-entry form will not be entitled to receive physical delivery of certificated Notes, except in certain limited circumstances. | |||||||

Form and Denomination | The Notes will be issued only in fully registered form without interest coupons in denominations of $25 and integral multiples of $25 in excess thereof. | |||||||

Trustee and Paying Agent | U.S. Bank National Association | |||||||

Governing Law | The indenture and the Notes will be governed by the laws of the State of New York. | |||||||

Risk Factors | ||||||||

14

RISK FACTORS

Investing in the Notes involves a number of significant risks. Before you invest in the Notes, you should be aware of various risks, including those described below. You should carefully consider these risk factors, together with all of the other information included in this prospectus, before you decide whether to make an investment in the Notes. The risks set out below present the principal risk factors associated with an investment in the Notes as well as those factors generally associated with investment in a company with investment objectives, investment policies, capital structure or trading markets similar to ours. Additional risks and uncertainties not presently known to us or not presently deemed material by us may also impair our operations and performance. If any of the following events were to occur, our business, financial condition, results of operations and cash flows could be materially and adversely affected. In such case, our business, financial condition and results of operations could be materially and adversely affected, and you may lose all or part of your investment.

Risk Factors Relating to this Offering and the Notes

The Notes will be structurally subordinated to the indebtedness and other liabilities of our future subsidiaries, if any.

The Notes will be obligations exclusively of Mount Logan Capital Inc., and not of any current or future subsidiaries, if any. None of our future subsidiaries will be a guarantor of the Notes and the Notes will not be required to be guaranteed by any subsidiary we may acquire or create in the future. Any assets of our subsidiaries will not be directly available to satisfy the claims of our creditors, including holders of the Notes. Except to the extent we are a creditor with recognized claims against our subsidiaries, all claims of creditors of our subsidiaries will have priority over our equity interests in such entities (and therefore the claims of our creditors, including holders of the Notes) with respect to the assets of such entities. Even if we are recognized as a creditor of one or more of these entities, our claims would still be effectively subordinated to any security interests in the assets of any such entity and to any indebtedness or other liabilities of any such entity senior to our claims. Consequently, the Notes will be structurally subordinated to all indebtedness and other liabilities of any of our future subsidiaries, if any. In addition, our future subsidiaries, if any, may incur substantial indebtedness in the future, all of which would be structurally senior to the Notes. Structural subordination means that creditors of a parent entity are subordinate to creditors of a subsidiary entity with respect to the subsidiary’s assets. Additionally, future debt and security agreements entered into by our subsidiaries, if any, may contain various restrictions, including restrictions on payments by our subsidiaries to us and the transfer by our subsidiaries of assets pledged as collateral.

Our amount of debt outstanding will increase as a result of this offering. Our future indebtedness could adversely affect our business, financial condition, results of operations, and ability to meet our payment obligations under the Notes and our other debt.

The use of debt and our level of indebtedness could have significant consequences on our future operations, including:

•making it more difficult for us to satisfy our obligations, including those relating to the Notes and our other outstanding indebtedness;

•making it more difficult for us to obtain additional debt or equity financing in the future;

•resulting in an event of default if we fail to comply with the financial and other restrictive covenants contained in our financing arrangements, which event of default could result in substantially all of our debt becoming immediately due and payable;

•reducing the availability of our cash flow to fund investments, acquisitions and other general corporate purposes, and limiting our ability to obtain additional financing for these purposes;

•subjecting us to the risk of increased sensitivity to interest rate increases on our indebtedness with variable interest rates, including borrowings under our financing arrangements;

•limiting our ability to refinance all or a portion of our indebtedness on or before maturity; and

15

•limiting our flexibility in planning for, or reacting to, and increasing our vulnerability to, downturns and other changes in our business, the industry in which we operate and the general economy.

Any of the above-listed factors could have an adverse effect on our business, financial condition and results of operations and our ability to meet our payment obligations under the Notes and our other debt.

Our ability to meet our payment and other obligations under our financing arrangements depends on our ability to generate significant cash flow in the future. This, to some extent, is subject to general economic, financial, competitive, legislative and regulatory factors as well as other factors that are beyond our control. We cannot assure you that our business will generate cash flow from operations, or that future borrowings will be available to us, in an amount sufficient to enable us to meet our payment obligations under the Notes and our other future debt and to fund other liquidity needs. If we are not able to generate sufficient cash flow to service our debt obligations, we may need to refinance or restructure our debt, including the Notes, sell assets, reduce or delay capital investments, or seek to raise additional capital. If we are unable to implement one or more of these alternatives, we may not be able to meet our payment obligations under the Notes and our other debt.

We may choose to redeem the Notes when prevailing interest rates are relatively low.

On or after , 20 , we may choose to redeem the Notes from time to time, especially when prevailing interest rates are lower than the rate borne by the Notes. If prevailing rates are lower at the time of redemption, you would not be able to reinvest the redemption proceeds in a comparable security at an effective interest rate as high as the interest rate on the Notes being redeemed. Our redemption right also may adversely impact your ability to sell the Notes as the optional redemption date or period approaches.

An increase in market interest rates could result in a decrease in the market value of the Notes.

The condition of the financial markets and prevailing interest rates have fluctuated in the past and are likely to fluctuate in the future, which could have an adverse effect on the market prices of the Notes. In general, as market interest rates rise, debt securities bearing interest at fixed rates of interest decline in value. Consequently, if you purchase Notes bearing interest at fixed rates and market interest rates increase, the market values of those Notes may decline. We cannot predict the future level of market interest rates.

The Notes will be unsecured and therefore will be effectively subordinated to our existing secured indebtedness and any secured indebtedness we may incur in the future.

The Notes will not be secured by any of our assets or any of the assets of our subsidiaries. As a result, the Notes are effectively subordinated to the currently existing secured indebtedness we or our subsidiaries have, including indebtedness under the Credit Facility, and any secured indebtedness we may incur in the future (or any indebtedness that is initially unsecured to which we subsequently grant security) to the extent of the value of the assets securing such indebtedness. In any liquidation, dissolution, bankruptcy or other similar proceeding, the holders of any of our existing or future secured indebtedness and the secured indebtedness of our subsidiaries may assert rights against the assets pledged to secure that indebtedness in order to receive full payment of their indebtedness before the assets may be used to pay other creditors, including the holders of the Notes.

The indenture under which the Notes will be issued contains limited protection for holders of the Notes.

The indenture under which the Notes will be issued offers limited protection to holders of the Notes. The terms of the indenture and the Notes do not restrict our or any of our subsidiaries or future subsidiaries’ ability to engage in, or otherwise be a party to, a variety of corporate transactions, circumstances or events that could have a material adverse impact on your investment in the Notes. In particular, the terms of the indenture and the Notes will not place any restrictions on our or our future subsidiaries’ ability to:

•issue securities or otherwise incur additional indebtedness or other obligations, including (1) any indebtedness or other obligations that would be equal in right of payment to the Notes, (2) any indebtedness or other obligations that would be secured and therefore rank effectively senior in right of payment to the Notes to the extent of the values of the assets securing such debt, (3) indebtedness of ours that is guaranteed

16

by one or more of our subsidiaries and which therefore is structurally senior to the Notes and (4) securities, indebtedness or obligations issued or incurred by our subsidiaries or the portfolio companies with respect to which we hold an equity investment that would be senior to our equity interests in those entities and therefore rank structurally senior to the Notes with respect to the assets of these entities, in each case other than an incurrence of indebtedness or other obligation that would cause a violation of Section 18(a)(1)(A) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time or any successor provisions (whether or not we are subject thereto), but giving effect, in each case, to any exemptive relief granted to us by the SEC.

•pay dividends on, or purchase or redeem or make any payments in respect of, capital stock or other securities ranking junior in right of payment to the Notes, including subordinated indebtedness, in each case other than dividends, purchases, redemptions or payments that would cause our asset coverage to fall below the threshold specified in Section 18(a)(1)(B) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time or any successor provisions, giving effect to (i) any exemptive relief granted to us by the SEC and (ii) no-action relief granted by the SEC to another BDC (or to us if we determine to seek such similar no-action or other relief) permitting the BDC to declare any cash dividend or distribution notwithstanding the prohibition contained in Section 18(a)(1)(B) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time in order to maintain the BDC’s status as a RIC. These provisions generally prohibit us from declaring any cash dividend or distribution upon any class of our capital stock, or purchasing any such capital stock if our asset coverage, as defined in the 1940 Act, is below 150% at the time of the declaration of the dividend or distribution or the purchase and after deducting the amount of such dividend, distribution or purchase;

•sell assets (other than certain limited restrictions on our ability to consolidate, merge or sell all or substantially all of our assets);

•enter into transactions with affiliates;

•create liens (including liens on the shares of any future subsidiaries) or enter into sale and leaseback transactions;

•make investments; or

•create restrictions on the payment of dividends or other amounts to us from any of our future subsidiaries.

In addition, the indenture does not require us to offer to purchase the Notes in connection with a change of control or any other event.

Furthermore, the terms of the indenture and the Notes do not protect holders of the Notes in the event that we experience changes (including significant adverse changes) in our financial condition, results of operations or credit ratings, if any, as they do not require that we adhere to any financial tests or ratios or specified levels of net worth, revenues, income, cash flow, or liquidity.

Our ability to recapitalize, incur additional debt and take a number of other actions that are not limited by the terms of the Notes may have important consequences for you as a holder of the Notes, including making it more difficult for us to satisfy our obligations with respect to the Notes or negatively affecting the trading value of the Notes.

Other debt we issue or incur in the future could contain more protections for its holders than the indenture and the Notes, including additional covenants and events of default. For example, the indenture under which the Notes are issued does not contain cross-default provisions. The issuance or incurrence of any such debt with incremental protections could affect the market for and trading levels and prices of the Notes.

17

Servicing our indebtedness will require a significant amount of cash. Our ability to generate sufficient cash depends on many factors, some of which are not within our control.

Our ability to make payments on, or refinance our obligations under, our indebtedness (including the Notes) and to fund planned capital expenditures will depend on our ability to generate cash in the future. To a certain extent, this is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. If we are unable to generate sufficient cash flow to service our debt and meet our other commitments, we may need to restructure or refinance all or a portion of our debt, sell material assets or operations or raise additional debt or equity capital. We may not be able to effect any of these actions on a timely basis, on commercially reasonable terms or at all, and these actions may not be sufficient to meet our capital requirements. In addition, the terms of our existing or future debt arrangements may restrict us from effecting any of these alternatives.

We may not be able to repurchase all of the Notes upon a Change of Control.

As described under “Description of Notes—Optional Redemption Upon Change of Control,” unless we have otherwise redeemed the Notes, we will be required to offer to repurchase the Notes upon the occurrence of a Change of Control with respect to the Notes. We may not have sufficient funds to repurchase the Notes for cash at such time. In addition, our ability to repurchase the Notes for cash may be limited or prohibited by law or our credit, lease or operating agreements in existence at the time. To the extent we are unable to obtain relief from any such limitations or prohibitions, we may be unable to repurchase the Notes. Regardless of the cause, our failure to offer to repurchase the Notes could constitute an event of default under the indenture which could, in turn, constitute a default under other of our agreements relating to our indebtedness outstanding at the time.

There is currently no market for the Notes, and we cannot assure you that an active trading market for the Notes will develop. The Notes may trade at prices below the price you paid for them.

The Notes are a new issue of debt securities for which there currently is no trading market. We intend to apply to list the Notes on The Nasdaq Global Market, and if the application is approved, we expect trading in the Notes on The Nasdaq Global Market to begin within 30 days of the original issue date. There is no assurance that the listing of the Notes on The Nasdaq Global Market will be approved. Even if the listing of the Notes is approved, we cannot provide any assurances that we will successfully list the Notes or that an active trading market will develop for the Notes. Further, we cannot provide any assurances as to the liquidity of any trading market that may develop for the Notes, your ability to sell your Notes or the price at which you will be able to sell your Notes, and you may have difficulty selling your Notes or may not be able to sell your Notes.. Future trading prices of the Notes will depend on many factors, including prevailing interest rates, general economic conditions, our financial condition and results of operations, the then-current ratings assigned to the Notes and the market for similar securities. Any trading market that develops may be affected by many factors independent of and in addition to the foregoing, including:

•time remaining prior to the maturity of the Notes;

•the outstanding amount of the Notes;

•the terms related to optional redemption of the Notes; and

•level, direction and volatility of market interest rates generally.

Certain of the underwriters have advised us that they presently intend to make a market in the Notes. However, they are not obligated to do so, and any market making with respect to the Notes may be discontinued without notice, in the underwriters’ sole discretion. Accordingly, a liquid trading market may not develop for the Notes, you may not be able to sell your Notes at a particular time and the price you receive when you sell may not be favorable. To the extent an active trading market does not develop, the liquidity and trading price for the Notes may be harmed. Therefore, you may be required to bear the financial risk of an investment in the Notes until maturity of the Notes. In addition, there may be a limited number of buyers when you decide to sell your Notes. This may affect the price, if any, offered for your Notes or your ability to sell your Notes when desired or at all.

18

If we default on our obligations to pay our other indebtedness, we may not be able to make payments on the Notes.

Any default under the agreements governing our indebtedness, including other indebtedness to which we may be a party that is not waived by the required lenders, and the remedies sought by the holders of such indebtedness could make us unable to pay principal, premium, if any, and interest on the Notes and substantially decrease the market value of the Notes. If we are unable to generate sufficient cash flow and are otherwise unable to obtain funds necessary to meet required payments of principal, premium, if any, and interest on our indebtedness, or if we otherwise fail to comply with the various covenants, including financial and operating covenants, in the instruments governing our indebtedness, we could be in default under the terms of the agreements governing such indebtedness. In the event of such default, the holders of such indebtedness could elect to declare all the funds borrowed thereunder to be due and payable, together with accrued and unpaid interest, the lenders under any other debt we may incur in the future could elect to terminate their commitments, cease making further loans and institute foreclosure proceedings against our assets, and we could be forced into bankruptcy or liquidation. If our operating performance declines, we may in the future need to seek to obtain waivers from the required lenders under other debt that we may incur in the future to avoid being in default. If we breach our covenants under other debt and seek a waiver, we may not be able to obtain a waiver from the required lenders. If this occurs, we would be in default under other debt, the lenders could exercise their rights as described above, and we could be forced into bankruptcy or liquidation. If we are unable to repay debt, lenders having secured obligations could proceed against the collateral securing the debt. See “Description of Notes” in this prospectus.

A downgrade, suspension or withdrawal of the credit rating assigned by a rating agency to us or the Notes, if any, or change in the debt markets could cause the liquidity or market value of the Notes to decline significantly.

Any credit ratings assigned by a rating agency to us are an assessment by rating agencies of our ability to pay our debts when due. Consequently, real or anticipated changes in our credit ratings will generally affect the market value of the Notes. These credit ratings may not reflect risks related to us and our business, suitability of a security for a particular investor and the structure or marketing of the Notes. Credit ratings are not a recommendation to buy, sell or hold any security, and may be revised or withdrawn at any time by the issuing organization in its sole discretion. Neither we nor any agent undertakes any obligation to maintain any credit ratings assigned to us or the Notes or to advise holders of Notes of any changes in our credit ratings. The conditions of the financial markets and prevailing interest rates have fluctuated in the past and are likely to fluctuate in the future, which could have an adverse effect on the market prices of the Notes. There can be no assurance that our credit ratings will remain for any given period of time or that such credit ratings will not be lowered or withdrawn entirely by the rating agency if in their judgment future circumstances relating to the basis of the credit ratings, such as adverse changes in our company, so warrant.

We have broad discretion in the use of the net proceeds of this offering and may not use them effectively.

We intend to use the net proceeds from this offering to repay borrowings under the Credit Agreement and any remainder for general corporate purposes. Our management will have broad discretion in the application of such remainder of net proceeds from this offering and could spend the proceeds in ways that do not improve our results of operations. The failure by management to apply these funds effectively could result in financial losses that could have a material adverse effect on our business and cause the price of the Notes to decline.

We may issue additional Notes.

The indenture governing the Notes will provide that we may from time to time, without notice to or the consent of the holders of the Notes, create and issue additional Notes which will be equal in rank to the Notes. We may issue such additional Notes, even if such issuance would not constitute a “qualified reopening” for U.S. federal income tax purposes.

19

Risks Related to Our Business – General

A portion of our revenues, earnings and cash flow is highly variable, which may make it difficult for it to achieve steady earnings growth on a quarterly basis and may cause the price of shares of our Common Stock to be volatile.

A portion of our revenues, earnings and cash flow is highly variable, primarily due to the nature of the insurance business of our subsidiary, Ability and the fact that fees from our asset management business vary significantly from quarter to quarter and year to year. We may also experience fluctuations in our results from quarter to quarter and year to year due to a number of other factors, including changes in our operating expenses, policyholder behavior, the degree to which we encounter competition and general economic and market conditions. Our future results will also be dependent on the success of the vehicles ML Management manages, changes in the value of which may result in fluctuations in our results. Such variability may lead to volatility in the trading price of shares of our common stock and cause our results for a particular period not to be indicative of our performance in a future period. It may be difficult for us to achieve steady growth in earnings and cash flow on a quarterly basis, which could in turn lead to adverse movements in the price of shares of our common stock or increased volatility in the price of shares of our common stock in general.

We operate in highly competitive industries, which could limit our ability to achieve our growth strategies and could materially and adversely affect our businesses, financial condition, results of operations, cash flows and prospects.

We operate in highly competitive markets and compete with a large number of investment management firms, private credit fund sponsors, U.S. and non-U.S. insurance and reinsurance companies and other financial institutions. In particular, our asset management business faces competition in the pursuit of clients, and our insurance business faces competition with respect to both the products we offer and insurance transactions we pursue. These competitive pressures may have a material and adverse effect on our growth, business, financial condition, results of operations, cash flows and prospects.

We rely on technology and information systems (including those of BCPA through our Servicing Agreement with BCPA), some of which are controlled by third-party vendors, to maintain the security of our information and technology networks and to conduct our business, and any failures or interruptions of these systems could adversely affect our business and results of operations.

We are subject to various risks and costs associated with the collection, handling, storage and transmission of proprietary or confidential information. In the ordinary course of business, we collect and store a range of data, including our proprietary business information and intellectual property, which may include personally identifiable information relating to our insurance business or of our employees, our investors, and other third parties, in data centers and on our or BCPA’s networks, and we rely on technology and information systems in our business activities. We rely on a host of information systems and hardware systems, including those of BCPA and BCPA’s third party vendors, for the secure processing, maintenance and transmission of this information, and the unavailability of these systems or the failure of these systems to perform as anticipated for any reason could disrupt our businesses and could result in decreased performance and increased operating costs, causing our businesses and results of operations to suffer.

There can be no assurance that the various procedures and controls we utilize to mitigate the threat of cyberattacks or other similar incidents will be sufficient to prevent disruptions to our systems, especially because the cyberattack techniques used change frequently and are not recognized until launched, the full scope of a cyberattack may not be realized until an investigation has been performed and cyberattacks can originate from a wide variety of sources. Although we and BCPA take protective measures to prevent and address potential cyberattacks, there can be no assurance that any of these measures will prove effective. The rapid evolution and increasing prevalence of artificial intelligence technologies may also increase our cybersecurity risks.

We rely on BCPA and third-party service providers for certain aspects of our businesses, including for certain information systems and technology. We cannot guarantee that BCPA, third party vendors, service providers and lenders have not been compromised or that they do not contain exploitable defects or bugs that could result in a

20

breach of or disruption to our information technology systems or the BCPA or third-party information technology systems that support our business. Our ability to monitor these third parties’ information security practices is limited, and they may not have adequate information security measures in place. In addition, if BCPA or one of our third-party counterparties suffers a security breach, Our response may be limited or more difficult because it may not have direct access to their systems. A disaster, disruption or compromise in technology or infrastructure that supports our businesses, including a disruption involving electronic communications or other services used by us, may have an adverse impact on our ability to continue to operate our businesses without interruption, which could have a material adverse effect on us. These risks could increase due to the increasing use of cloud-based software services. In addition, costs related to data security threats or disruptions may not be fully insured or indemnified by other means.

As new technologies, including tools that harness generative artificial intelligence and other machine learning techniques, rapidly develop and become even more accessible, the use of such new technologies by us, our affiliates and our third party service providers and other vendors will present additional known and unknown risks, including, among others, the risk that confidential information may be stolen, misappropriated or disclosed and the risk that we and/or our third party service providers or other vendors may rely on incorrect, unclear or biased outputs generated by such technologies, any of which could have an adverse impact on us and our business.

A significant actual or potential theft, loss, corruption, exposure, fraudulent, unauthorized or accidental use or misuse of personally identifiable or proprietary business data could result in significant remediation and other costs, fines, litigation and regulatory actions against us, in addition to significant reputational harm.

Our business, financial condition, results of operations, liquidity and cash flows will depend on the accuracy of our management’s assumptions and estimates, and we could experience significant gains or losses if these assumptions and estimates differ significantly from actual results.